Page 48 - Chap7 ITC

P. 48

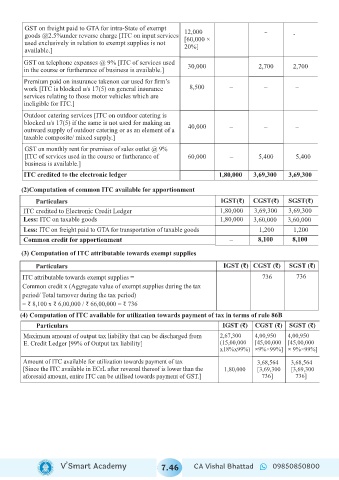

GST on freight paid to GTA for intra-State of exempt 12,000

goods @2.5%under reverse charge [ITC on input services [60,000 × – -

used exclusively in relation to exempt supplies is not 20%]

available.]

GST on telephone expenses @ 9% [ITC of services used

in the course or furtherance of business is available.] 30,000 2,700 2,700

Premium paid on insurance takenon car used for firm’s

work [ITC is blocked u/s 17(5) on general insurance 8,500 – – –

services relating to those motor vehicles which are

ineligible for ITC.]

Outdoor catering services [ITC on outdoor catering is

blocked u/s 17(5) if the same is not used for making an 40,000 – – –

outward supply of outdoor catering or as an element of a

taxable composite/ mixed supply.]

GST on monthly rent for premises of sales outlet @ 9%

[ITC of services used in the course or furtherance of 60,000 – 5,400 5,400

business is available.]

ITC credited to the electronic ledger 1,80,000 3,69,300 3,69,300

(2)Computation of common ITC available for apportionment

Particulars IGST( )₹ CGST(₹) SGST(₹)

ITC credited to Electronic Credit Ledger 1,80,000 3,69,300 3,69,300

Less: ITC on taxable goods 1,80,000 3,60,000 3,60,000

Less: ITC on freight paid to GTA for transportation of taxable goods 1,200 1,200

Common credit for apportionment – 8,100 8,100

(3) Computation of ITC attributable towards exempt supplies

Particulars IGST ( )₹ CGST ( )₹ SGST ( )₹

ITC attributable towards exempt supplies = 736 736

Common credit x (Aggregate value of exempt supplies during the tax

period/ Total turnover during the tax period)

= ₹ 8,100 x ₹ 6,00,000 / ₹ 66,00,000 = ₹ 736

(4) Computation of ITC available for utilization towards payment of tax in terms of rule 86B

Particulars IGST (₹) CGST (₹) SGST (₹)

Maximum amount of output tax liability that can be discharged from 2,67,300 4,00,950 4,00,950

E. Credit Ledger [99% of Output tax liability] (15,00,000 [45,00,000 [45,00,000

x18%x99%) ×9%×99%] × 9%×99%]

Amount of ITC available for utilization towards payment of tax 3,68,564 3,68,564

[Since the ITC available in ECrL after reversal thereof is lower than the 1,80,000 [3,69,300 [3,69,300

aforesaid amount, entire ITC can be utilised towards payment of GST.] – 736] – 736]

V’Smart Academy 7.46 CA Vishal Bhattad 09850850800