Page 45 - Chap7 ITC

P. 45

(ii) The restrictions can be imposed under the following circumstances: -

(a) ITC has been availed on the basis of tax invoices/valid documents -

Ü issued by a non-existent supplier or by a person not conducting any business from the registered place

of business or

Ü without receipt of goods or services or both or

Ü the tax in relation to which has not been paid to the Government

(b) Registered person availing ITC has been found non-existent or not to be conducting any business from the

registered place of business or

(c) Registered person availing ITC is not in possession of valid tax invoice.

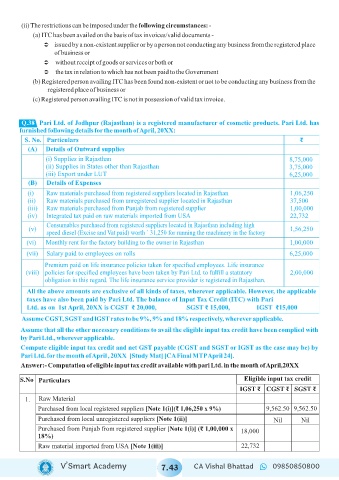

Q.38 Pari Ltd. of Jodhpur (Rajasthan) is a registered manufacturer of cosmetic products. Pari Ltd. has

furnished following details for the month of April, 20XX:

S. No. Particulars ₹

(A) Details of Outward supplies

(i) Supplies in Rajasthan 8,75,000

(ii) Supplies in States other than Rajasthan 3,75,000

(iii) Export under LUT 6,25,000

(B) Details of Expenses

(i) Raw materials purchased from registered suppliers located in Rajasthan 1,06,250

(ii) Raw materials purchased from unregistered supplier located in Rajasthan 37,500

(iii) Raw materials purchased from Punjab from registered supplier 1,00,000

(iv) Integrated tax paid on raw materials imported from USA 22,732

Consumables purchased from registered suppliers located in Rajasthan including high

(v) 1,56,250

speed diesel (Excise and Vat paid) worth ` 31,250 for running the machinery in the factory

(vi) Monthly rent for the factory building to the owner in Rajasthan 1,00,000

(vii) Salary paid to employees on rolls 6,25,000

Premium paid on life insurance policies taken for specified employees. Life insurance

(viii) policies for specified employees have been taken by Pari Ltd. to fulfill a statutory 2,00,000

obligation in this regard. The life insurance service provider is registered in Rajasthan.

All the above amounts are exclusive of all kinds of taxes, wherever applicable. However, the applicable

taxes have also been paid by Pari Ltd. The balance of Input Tax Credit (ITC) with Pari

Ltd. as on 1st April, 20XX is CGST ₹ 20,000, SGST ₹ 15,000, IGST ₹15,000

Assume CGST, SGST and lGST rates to be 9%, 9% and 18% respectively, wherever applicable.

Assume that all the other necessary conditions to avail the eligible input tax credit have been complied with

by Pari Ltd., wherever applicable.

Compute eligible input tax credit and net GST payable (CGST and SGST or IGST as the case may be) by

Pari Ltd. for the month of April , 20XX [Study Mat] [CA Final MTP April 24].

Answer:- Computation of eligible input tax credit available with pari Ltd. in the month of April,20XX

S.No Particulars Eligible input tax credit

IGST ₹ CGST ₹ SGST ₹

1. Raw Material

Purchased from local registered suppliers [Note 1(i)](₹ 1,06,250 x 9%) 9,562.50 9,562.50

Purchased from local unregistered suppliers [Note 1(ii)] Nil Nil

Purchased from Punjab from registered supplier [Note 1(i)] (₹ 1,00,000 x

18,000

18%)

Raw material imported from USA [Note 1(iii)] 22,732

V’Smart Academy 7.43 CA Vishal Bhattad 09850850800