Page 44 - Chap7 ITC

P. 44

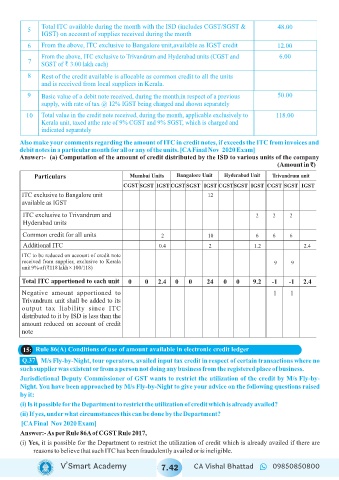

Total ITC available during the month with the ISD (includes CGST/SGST & 48.00

5

IGST) on account of supplies received during the month

6 From the above, ITC exclusive to Bangalore unit,available as IGST credit 12.00

From the above, ITC exclusive to Trivandrum and Hyderabad units (CGST and 6.00

7

SGST of ` 3.00 lakh each)

8 Rest of the credit available is allocable as common credit to all the units

and is received from local suppliers in Kerala.

9 Basic value of a debit note received, during the month,in respect of a previous 50.00

supply, with rate of tax @ 12% IGST being charged and shown separately

10 Total value in the credit note received, during the month, applicable exclusively to 118.00

Kerala unit, taxed atthe rate of 9% CGST and 9% SGST, which is charged and

indicated separately

Also make your comments regarding the amount of ITC in credit notes, if exceeds the ITC from invoices and

debit notes in a particular month for all or any of the units. [CA Final Nov 2020 Exam]

Answer:- (a) Computation of the amount of credit distributed by the ISD to various units of the company

(Amount in ₹)

Particulars Mumbai Units Bangalore Unit Hyderabad Unit Trivandrum unit

CGST SGST IGST CGST SGST IGST CGSTSGST IGST CGST SGST IGST

ITC exclusive to Bangalore unit 12

available as IGST

ITC exclusive to Trivandrum and 2 2 2

Hyderabad units

Common credit for all units 2 10 6 6 6

Additional ITC 0.4 2 1.2 2.4

ITC to be reduced on account of credit note

received from supplier, exclusive to Kerala 9 9

unit 9% of (₹118 lakh × 100/118)

Total ITC apportioned to each unit 0 0 2.4 0 0 24 0 0 9.2 -1 -1 2.4

Negative amount apportioned to 1 1

Trivandrum unit shall be added to its

output tax liability since ITC

distributed to it by ISD is less than the

amount reduced on account of credit

note

15: Rule 86(A) Conditions of use of amount available in electronic credit ledger

Q.37

M/s Fly-by-Night, tour operators, availed input tax credit in respect of certain transactions where no

such supplier was existent or from a person not doing any business from the registered place of business.

Jurisdictional Deputy Commissioner of GST wants to restrict the utilization of the credit by M/s Fly-by-

Night. You have been approached by M/s Fly-by-Night to give your advice on the following questions raised

by it:

(i) Is it possible for the Department to restrict the utilization of credit which is already availed?

(ii) If yes, under what circumstances this can be done by the Department?

[CA Final Nov 2020 Exam]

Answer:- As per Rule 86A of CGST Rule 2017,

(i) Yes, it is possible for the Department to restrict the utilization of credit which is already availed if there are

reasons to believe that such ITC has been fraudulently availed or is ineligible.

V’Smart Academy 7.42 CA Vishal Bhattad 09850850800