Page 47 - Chap7 ITC

P. 47

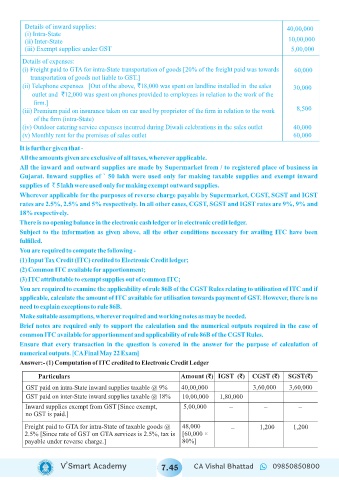

Details of inward supplies: 40,00,000

(i) Intra-State

(ii) Inter-State 10,00,000

(iii) Exempt supplies under GST 5,00,000

Details of expenses:

(i) Freight paid to GTA for intra-State transportation of goods [20% of the freight paid was towards 60,000

transportation of goods not liable to GST.]

(ii) Telephone expenses [Out of the above, 18,000 was spent on landline installed in the sales ` 30,000

outlet and 12,000 was spent on phones provided to employees in relation to the work of the `

firm.]

(iii) Premium paid on insurance taken on car used by proprietor of the firm in relation to the work 8,500

of the firm (intra-State)

(iv) Outdoor catering service expenses incurred during Diwali celebrations in the sales outlet 40,000

(v) Monthly rent for the premises of sales outlet 60,000

It is further given that -

All the amounts given are exclusive of all taxes, wherever applicable.

All the inward and outward supplies are made by Supermarket from / to registered place of business in

Gujarat. Inward supplies of ` 50 lakh were used only for making taxable supplies and exempt inward

supplies of ` 5 lakh were used only for making exempt outward supplies.

Wherever applicable for the purposes of reverse charge payable by Supermarket, CGST, SGST and IGST

rates are 2.5%, 2.5% and 5% respectively. In all other cases, CGST, SGST and IGST rates are 9%, 9% and

18% respectively.

There is no opening balance in the electronic cash ledger or in electronic credit ledger.

Subject to the information as given above, all the other conditions necessary for availing ITC have been

fulfilled.

You are required to compute the following -

(1) Input Tax Credit (ITC) credited to Electronic Credit ledger;

(2) Common ITC available for apportionment;

(3) ITC attributable to exempt supplies out of common ITC;

You are required to examine the applicability of rule 86B of the CGST Rules relating to utilisation of ITC and if

applicable, calculate the amount of ITC available for utilisation towards payment of GST. However, there is no

need to explain exceptions to rule 86B.

Make suitable assumptions, wherever required and working notes as may be needed.

Brief notes are required only to support the calculation and the numerical outputs required in the case of

common ITC available for apportionment and applicability of rule 86B of the CGST Rules.

Ensure that every transaction in the question is covered in the answer for the purpose of calculation of

numerical outputs. [CA Final May 22 Exam]

Answer:- (1) Computation of ITC credited to Electronic Credit Ledger

Particulars Amount (₹) IGST (₹) CGST (₹) SGST(₹)

GST paid on intra-State inward supplies taxable @ 9% 40,00,000 3,60,000 3,60,000

GST paid on inter-State inward supplies taxable @ 18% 10,00,000 1,80,000

Inward supplies exempt from GST [Since exempt, 5,00,000 – – –

no GST is paid.]

Freight paid to GTA for intra-State of taxable goods @ 48,000 – 1,200 1,200

2.5% [Since rate of GST on GTA services is 2.5%, tax is [60,000 ×

payable under reverse charge.] 80%]

V’Smart Academy 7.45 CA Vishal Bhattad 09850850800