Page 46 - Chap7 ITC

P. 46

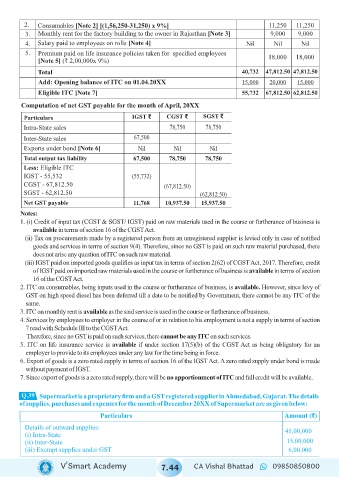

2. Consumables [Note 2] [(1,56,250-31,250) x 9%] 11,250 11,250

3. Monthly rent for the factory building to the owner in Rajasthan [Note 3] 9,000 9,000

4. Salary paid to employees on rolls [Note 4] Nil Nil Nil

5. Premium paid on life insurance policies taken for specified employees 18,000 18,000

[Note 5] (₹ 2,00,000x 9%)

Total 40,732 47,812.50 47,812.50

Add: Opening balance of ITC on 01.04.20XX 15,000 20,000 15,000

Eligible ITC [Note 7] 55,732 67,812.50 62,812.50

Computation of net GST payable for the month of April, 20XX

Particulars IGST ₹ CGST ₹ SGST ₹

Intra-State sales 78,750 78,750

Inter-State sales 67,500

Exports under bond [Note 6] Nil Nil Nil

Total output tax liability 67,500 78,750 78,750

Less: Eligible ITC

IGST - 55,532 (55,732)

CGST - 67,812.50 (67,812.50)

SGST - 62,812.50 (62,812.50)

Net GST payable 11,768 10,937.50 15,937.50

Notes:

1. (i) Credit of input tax (CGST & SGST/ IGST) paid on raw materials used in the course or furtherance of business is

available in terms of section 16 of the CGST Act.

(ii) Tax on procurements made by a registered person from an unregistered supplier is levied only in case of notified

goods and services in terms of section 9(4). Therefore, since no GST is paid on such raw material purchased, there

does not arise any question of ITC on such raw material.

(iii) IGST paid on imported goods qualifies as input tax in terms of section 2(62) of CGST Act, 2017. Therefore, credit

of IGST paid on imported raw materials used in the course or furtherance of business is available in terms of section

16 of the CGST Act.

2. ITC on consumables, being inputs used in the course or furtherance of business, is available. However, since levy of

GST on high speed diesel has been deferred till a date to be notified by Government, there cannot be any ITC of the

same.

3. ITC on monthly rent is available as the said service is used in the course or furtherance of business.

4. Services by employees to employer in the course of or in relation to his employment is not a supply in terms of section

7 read with Schedule III to the CGST Act.

Therefore, since no GST is paid on such services, there cannot be any ITC on such services.

5. ITC on life insurance service is available if under section 17(5)(b) of the CGST Act as being obligatory for an

employer to provide to its employees under any law for the time being in force.

6. Export of goods is a zero rated supply in terms of section 16 of the IGST Act. A zero rated supply under bond is made

without payment of IGST.

7. Since export of goods is a zero rated supply, there will be no apportionment of ITC and full credit will be available.

Q.39

Supermarket is a proprietary firm and a GST registered supplier in Ahmedabad, Gujarat. The details

of supplies, purchases and expenses for the month of December 20XX of Supermarket are as given below:

Particulars Amount (₹)

Details of outward supplies: 45,00,000

(i) Intra-State

(ii) Inter-State 15,00,000

(iii) Exempt supplies under GST 6,00,000

V’Smart Academy 7.44 CA Vishal Bhattad 09850850800