Page 6 - Chapter 14 Return.cdr

P. 6

CCP 14.04.11.00

CCP 14.03.09.00

If a return has been filed, how can it be revised if some changes are required to Mr. P has opted for QRMP Scheme and wants to know how to declare details and

be made? (ICAI Material)(CA Inter MTP Mar 19) OR file returns under this scheme. You are requested to guide Mr. P on procedure to

Explain the provisions of section 39(9) of the CGST Act, 2017 with reference to be followed.

rectification of returns. [CA Final RTP May 19] Answer:-

Answer: In GST since the returns are built from details of individual transactions, 1. Mr. P is required to submit details of outward supplies in IFF(Invoice Furnishing

there is no requirement for having a revised return. Facility) for 1st and 2nd month by 13th of the following month.

As per section 39(9) of the CGST Act, 2017, if any registered person after 2. Furnishing details in IFF is optional and the value of supply declared in IFF shall

CH 14

furnishing a return discovers any omission or incorrect particulars therein, he shall not exceed `50 lakhs in each month

rectify such omission or incorrect particulars in the return to be furnished for the 3. GSTR 1 has to be compulsorily filed after end of quarter by 13th of next month.

Return month or quarter during which such omission or incorrect particulars are noticed, 4. The details of invoices furnished in IFF in first 2 months need not be again

declared in GSTR 1

subject to payment of interest.

However, section 39(9) does not permit rectification of error or omission 5. Payment of Tax is to be made by using Challan PMT-06 by 25th of succeeding

discovered on account of scrutiny, audit, inspection or enforcement activities by tax month for first two months and for the last month along with filing of return

authorities. GSTR 3B

Further, no such rectification of any omission or incorrect particulars shall be 6. Mr. P can make such payment using any of the methods namely, Fixed Sum

allowed after the due date for furnishing of return for the month of September or Method or Self-Assessment method.

second quarter following the end of the financial year, or the actual date of furnishing 7. The 3B has to be filed by 22nd / 24th day of month succeeding end of quarter.

of relevant annual return, whichever is earlier

04. QRMP Scheme CCP 14.04.12.00

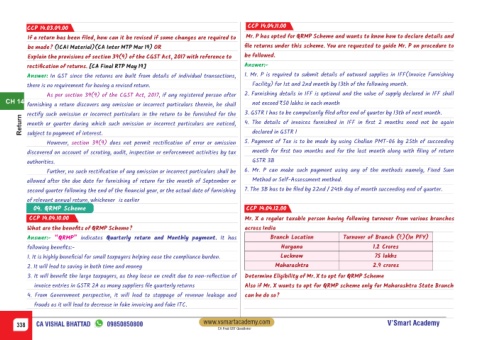

CCP 14.04.10.00 Mr. X a regular taxable person having following turnover from various branches

What are the benefits of QRMP Scheme? across India

Answer:- “QRMP” indicates Quarterly return and Monthly payment. It has Branch Location Turnover of Branch (`)(In PFY)

following benefits:- Haryana 1.2 Crores

1. It is highly beneficial for small taxpayers helping ease the compliance burden. Lucknow 75 lakhs

2. It will lead to saving in both time and money Maharashtra 2.9 crores

3. It will benefit the large taxpayers, as they loose on credit due to non-reflection of Determine Eligibility of Mr. X to opt for QRMP Scheme

invoice entries in GSTR 2A as many suppliers file quarterly returns Also if Mr. X wants to opt for QRMP scheme only for Maharashtra State Branch

4. From Government perspective, it will lead to stoppage of revenue leakage and can he do so?

frauds as it will lead to decrease in fake invoicing and fake ITC.

www.vsmartacademy.com

338 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner