Page 8 - Chapter 14 Return.cdr

P. 8

Answer:-SAM is a method for computation of payment of tax, for the person, who Answer:-

opts for QRMP scheme. SAM stands for "Self-Assessment Method", where the (I) Mr.B can opt out of the scheme voluntarily by using the facility to opt out for the

taxpayer can pay the tax liability by considering the tax liabilities on inward and quarter which is available from 1st day of second month of preceding quarter to

outward supplies and as per the ITC available. last day of first month of quarter.

Based on the above provision, Payment of tax for the month of May XX will be as Mr.B has to apply for opting out from 01.05.2021 to 31 .07.2021.

follows:- (ii) If Turnover crosses 5 crore Mr.B is compulsorily required to opt out of the scheme.

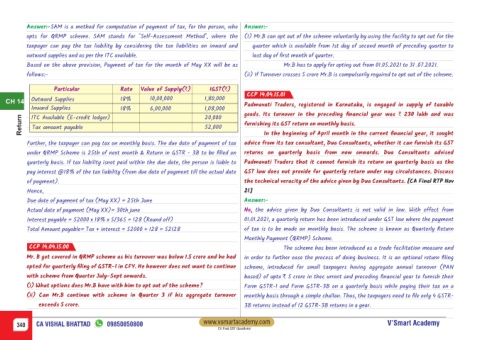

Particular Rate Value of Supply(`) IGST(`)

CCP 14.04.15.01

CH 14 Outward Supplies 18% 10,00,000 1,80,000

Inward Supplies 18% 6,00,000 1,08,000 Padmavati Traders, registered in Karnataka, is engaged in supply of taxable

goods. Its turnover in the preceding financial year was ` 230 lakh and was

Return Tax amount payable 52,000 furnishing its GST return on monthly basis.

ITC Available (E-credit ledger)

20,000

In the beginning of April month in the current financial year, it sought

Further, the taxpayer can pay tax on monthly basis. The due date of payment of tax advice from its tax consultant, Dua Consultants, whether it can furnish its GST

under QRMP Scheme is 25th of next month & Return in GSTR - 3B to be filled on returns on quarterly basis from now onwards. Dua Consultants advised

quarterly basis. If tax liability isnot paid within the due date, the person is liable to Padmavati Traders that it cannot furnish its return on quarterly basis as the

pay interest @18% of the tax liability (from due date of payment till the actual date GST law does not provide for quarterly return under nay circulstances. Discuss

of payment). the technical veracity of the advice given by Dua Consultants. [CA Final RTP Nov

Hence, 21]

Due date of payment of tax (May XX) = 25th June Answer:-

Actual date of payment (May XX)= 30th june No, the advice given by Dua Consultants is not valid in law. With effect from

Interest payable = 52000 x 18% x 5/365 = 128 (Round off) 01.01.2021, a quarterly return has been introduced under GST law where the payment

Total Amount payable= Tax + interest = 52000 + 128 = 52128 of tax is to be made on monthly basis. The scheme is known as Quarterly Return

Monthly Payment (QRMP) Scheme.

CCP 14.04.15.00 The scheme has been introduced as a trade facilitation measure and

Mr. B got covered in QRMP scheme as his turnover was below 1.5 crore and he had in order to further ease the process of doing business. It is an optional return filing

opted for quarterly filing of GSTR-1 in CFY. He however does not want to continue scheme, introduced for small taxpayers having aggregate annual turnover (PAN

with scheme from Quarter July-Sept onwards. based) of upto ` 5 crore in thec urrent and preceding financial year to furnish their

(i) What options does Mr.B have with him to opt out of the scheme? Form GSTR-1 and Form GSTR-3B on a quarterly basis while paying their tax on a

(ii) Can Mr.B continue with scheme in Quarter 3 if his aggregate turnover monthly basis through a simple challan. Thus, the taxpayers need to file only 4 GSTR-

exceeds 5 crore. 3B returns instead of 12 GSTR-3B returns in a year.

www.vsmartacademy.com

340 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner