Page 27 - Chapter 2.cdr

P. 27

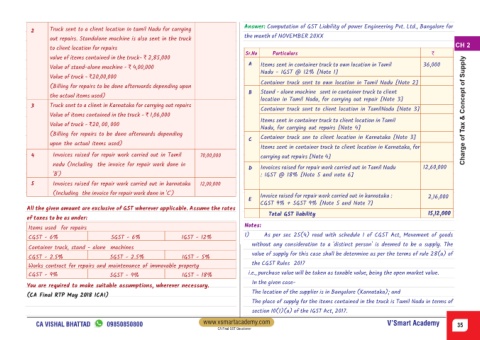

Answer: Computation of GST Liability of power Engineering Pvt. Ltd., Bangalore for

2 Truck sent to a client location in tamil Nadu for carrying

the month of NOVEMBER 20XX

out repairs. Standalone machine is also sent in the truck

CH 2

to client location for repairs

Sr.No Particulars `

value of items contained in the truck- ` 2,85,000

A Items sent in container truck to own location in Tamil 36,000

Value of stand-alone machine - ` 4,00,000

Nadu - IGST @ 12% [Note 1]

Value of truck - `20,00,000

Container truck sent to own location in Tamil Nadu [Note 2]

(Billing for repairs to be done afterwards depending upon

B Stand - alone machine sent in container truck to client

the actual items used)

location in Tamil Nadu, for carrying out repair [Note 3]

3 Truck sent to a client in Karnataka for carrying out repairs

Container truck sent to client location in TamilNadu [Note 3] Charge of Tax & Concept of Supply

Value of items contained in the truck - ` 1,06,000

Items sent in container truck to client location in Tamil

Value of truck - `20, 00, 000

Nadu, for carrying out repairs [Note 4]

(Billing for repairs to be done afterwards depending

C Container truck sen to client location in Karnataka [Note 3]

upon the actual items used)

Items sent in container truck to client location in Karnataka, for

4 Invoices raised for repair work carried out in Tamil 70,00,000 carrying out repairs [Note 4]

nadu (Including the invoice for repair work done in

D Invoices raised for repair work carried out in Tamil Nadu 12,60,000

'B') : IGST @ 18% [Note 5 and note 6]

5 Invoices raised for repair work carried out in karnataka 12,00,000

(Including the invoice for repair work done in 'C') Invoice raised for repair work carried out in karnataka :

E 2,16,000

CGST 9% + SGST 9% [Note 5 and Note 7]

All the given amount are exclusive of GST wherever applicable. Assume the rates

Total GST liability 15,12,000

of taxes to be as under:

Notes:

Items used for repairs

1) As per sec 25(4) read with schedule I of CGST Act, Movement of goods

CGST - 6% SGST - 6% IGST - 12%

without any consideration to a 'distinct person' is deemed to be a supply. The

Container truck, stand - alone machines

value of supply for this case shall be determine as per the terms of rule 28(a) of

CGST - 2.5% SGST - 2.5% IGST - 5%

the CGST Rules 2017

Works contract for repairs and maintenance of immovable property

CGST - 9% SGST - 9% IGST - 18% i.e., purchase value will be taken as taxable value, being the open market value.

In the given case-

You are required to make suitable assumptions, wherever necessary.

The location of the supplier is in Bangalore (Karnataka); and

(CA Final RTP May 2018 ICAI)

The place of supply for the items contained in the truck is Tamil Nadu in terms of

section 10(1)(a) of the IGST Act, 2017.

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 35

CA Final GST Questioner