Page 5 - 10. COMPILER QB - INDAS 36

P. 5

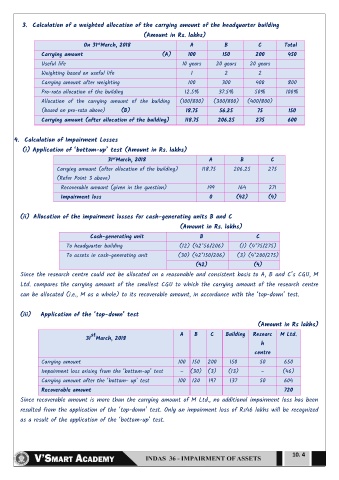

3. Calculation of a weighted allocation of the carrying amount of the headquarter building

(Amount in Rs. lakhs)

On 31 March, 2018 A B C Total

st

Carrying amount (A) 100 150 200 450

Useful life 10 years 20 years 20 years

Weighting based on useful life 1 2 2

Carrying amount after weighting 100 300 400 800

Pro-rata allocation of the building 12.5% 37.5% 50% 100%

Allocation of the carrying amount of the building (100/800) (300/800) (400/800)

(based on pro-rata above) (B) 18.75 56.25 75 150

Carrying amount (after allocation of the building) 118.75 206.25 275 600

4. Calculation of Impairment Losses

(i) Application of ‘bottom-up’ test (Amount in Rs. lakhs)

st

31 March, 2018 A B C

Carrying amount (after allocation of the building) 118.75 206.25 275

(Refer Point 3 above)

Recoverable amount (given in the question) 199 164 271

Impairment loss 0 (42) (4)

(ii) Allocation of the impairment losses for cash-generating units B and C

(Amount in Rs. lakhs)

Cash-generating unit B C

To headquarter building (12) (42*56/206) (1) (4*75/275)

To assets in cash-generating unit (30) (42*150/206) (3) (4*200/275)

(42) (4)

Since the research centre could not be allocated on a reasonable and consistent basis to A, B and C’s CGU, M

Ltd. compares the carrying amount of the smallest CGU to which the carrying amount of the research centre

can be allocated (i.e., M as a whole) to its recoverable amount, in accordance with the ‘top-down’ test.

(iii) Application of the ‘top-down’ test

(Amount in Rs lakhs)

st A B C Building Researc M Ltd.

31 March, 2018

h

centre

Carrying amount 100 150 200 150 50 650

Impairment loss arising from the ‘bottom-up’ test – (30) (3) (13) – (46)

Carrying amount after the ‘bottom- up’ test 100 120 197 137 50 604

Recoverable amount 720

Since recoverable amount is more than the carrying amount of M Ltd., no additional impairment loss has been

resulted from the application of the ‘top-down’ test. Only an impairment loss of Rs46 lakhs will be recognized

as a result of the application of the ‘bottom-up’ test.

10. 4