Page 10 - 10. COMPILER QB - INDAS 36

P. 10

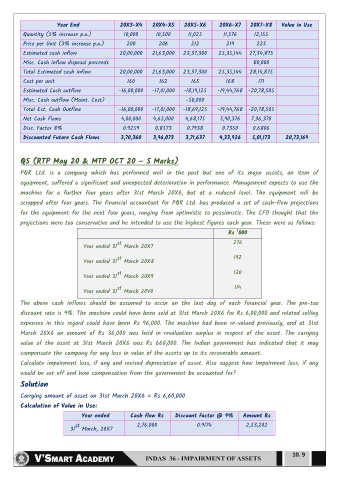

Year End 20X3-X4 20X4-X5 20X5-X6 20X6-X7 20X7-X8 Value in Use

Quantity (5% increase p.a.) 10,000 10,500 11,025 11,576 12,155

Price per Unit (3% increase p.a.) 200 206 212 219 225

Estimated cash inflow 20,00,000 21,63,000 23,37,300 25,35,144 27,34,875

Misc. Cash inflow disposal proceeds 80,000

Total Estimated cash inflow 20,00,000 21,63,000 23,37,300 25,35,144 28,14,875

Cost per unit 160 162 165 168 171

Estimated Cash outflow -16,00,000 -17,01,000 -18,19,125 -19,44,768 -20,78,505

Misc. Cash outflow (Maint. Cost) -50,000

Total Est. Cash Outflow -16,00,000 -17,01,000 -18,69,125 -19,44,768 -20,78,505

Net Cash Flows 4,00,000 4,62,000 4,68,175 5,90,376 7,36,370

Disc. Factor 8% 0.9259 0.8573 0.7938 0.7350 0.6806

Discounted Future Cash Flows 3,70,360 3,96,073 3,71,637 4,33,926 5,01,173 20,73,169

Q5 (RTP May 20 & MTP OCT 20 – 5 Marks)

PQR Ltd. is a company which has performed well in the past but one of its major assets, an item of

equipment, suffered a significant and unexpected deterioration in performance. Management expects to use the

machine for a further four years after 31st March 20X6, but at a reduced level. The equipment will be

scrapped after four years. The financial accountant for PQR Ltd. has produced a set of cash-flow projections

for the equipment for the next four years, ranging from optimistic to pessimistic. The CFO thought that the

projections were too conservative and he intended to use the highest figures each year. These were as follows:

Rs ʼ000

st 276

Year ended 31 March 20X7

st 192

Year ended 31 March 20X8

st 120

Year ended 31 March 20X9

st 114

Year ended 31 March 20Y0

The above cash inflows should be assumed to occur on the last day of each financial year. The pre-tax

discount rate is 9%. The machine could have been sold at 31st March 20X6 for Rs 6,00,000 and related selling

expenses in this regard could have been Rs 96,000. The machine had been re-valued previously, and at 31st

March 20X6 an amount of Rs 36,000 was held in revaluation surplus in respect of the asset. The carrying

value of the asset at 31st March 20X6 was Rs 660,000. The Indian government has indicated that it may

compensate the company for any loss in value of the assets up to its recoverable amount.

Calculate impairment loss, if any and revised depreciation of asset. Also suggest how Impairment loss, if any

would be set off and how compensation from the government be accounted for?

Solution

Carrying amount of asset on 31st March 20X6 = Rs 6,60,000

Calculation of Value in Use:

Year ended Cash flow Rs Discount factor @ 9% Amount Rs

st 2,76,000 0.9174 2,53,202

31 March, 20X7

10. 9