Page 12 - 2. COMPILER QB - INDAS 12

P. 12

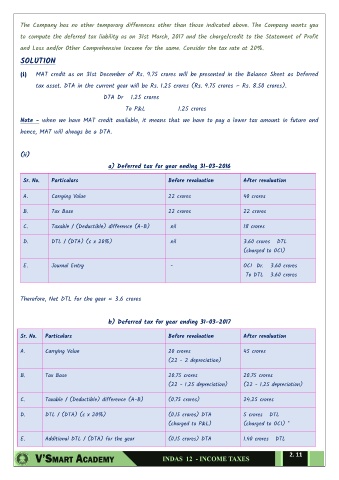

The Company has no other temporary differences other than those indicated above. The Company wants you

to compute the deferred tax liability as on 31st March, 2017 and the charge/credit to the Statement of Profit

and Loss and/or Other Comprehensive Income for the same. Consider the tax rate at 20%.

SOLUTION

(i) MAT credit as on 31st December of Rs. 9.75 crores will be presented in the Balance Sheet as Deferred

tax asset. DTA in the current year will be Rs. 1.25 crores (Rs. 9.75 crores – Rs. 8.50 crores).

DTA Dr 1.25 crores

To P&L 1.25 crores

Note - when we have MAT credit available, it means that we have to pay a lower tax amount in future and

hence, MAT will always be a DTA.

(ii)

a) Deferred tax for year ending 31-03-2016

Sr. No. Particulars Before revaluation After revaluation

A. Carrying Value 22 crores 40 crores

B. Tax Base 22 crores 22 crores

C. Taxable / (Deductible) difference (A-B) nil 18 crores

D. DTL / (DTA) (c x 20%) nil 3.60 crores DTL

(charged to OCI)

E. Journal Entry - OCI Dr. 3.60 crores

To DTL 3.60 crores

Therefore, Net DTL for the year = 3.6 crores

b) Deferred tax for year ending 31-03-2017

Sr. No. Particulars Before revaluation After revaluation

A. Carrying Value 20 crores 45 crores

(22 - 2 depreciation)

B. Tax Base 20.75 crores 20.75 crores

(22 - 1.25 depreciation) (22 - 1.25 depreciation)

C. Taxable / (Deductible) difference (A-B) (0.75 crores) 24.25 crores

D. DTL / (DTA) (c x 20%) (0.15 crores) DTA 5 crores DTL

(charged to P&L) (charged to OCI) *

E. Additional DTL / (DTA) for the year (0.15 crores) DTA 1.40 crores DTL

2. 11