Page 9 - 2. COMPILER QB - INDAS 12

P. 9

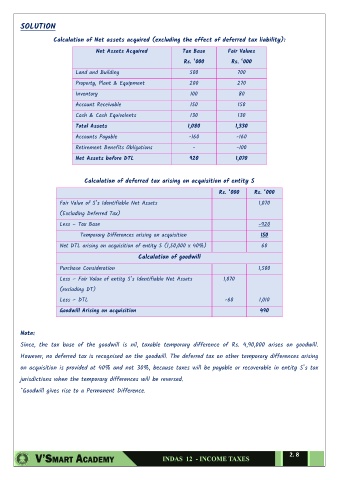

SOLUTION

Calculation of Net assets acquired (excluding the effect of deferred tax liability):

Net Assets Acquired Tax Base Fair Values

Rs. ‘000 Rs. ‘000

Land and Building 500 700

Property, Plant & Equipment 200 270

Inventory 100 80

Account Receivable 150 150

Cash & Cash Equivalents 130 130

Total Assets 1,080 1,330

Accounts Payable -160 -160

Retirement Benefits Obligations - -100

Net Assets before DTL 920 1,070

Calculation of deferred tax arising on acquisition of entity S

Rs. ‘000 Rs. ‘000

Fair Value of S’s Identifiable Net Assets 1,070

(Excluding Deferred Tax)

Less – Tax Base -920

Temporary Differences arising on acquisition 150

Net DTL arising on acquisition of entity S (1,50,000 x 40%) 60

Calculation of goodwill

Purchase Consideration 1,500

Less – Fair Value of entity S’s Identifiable Net Assets 1,070

(excluding DT)

Less – DTL -60 1,010

Goodwill Arising on acquisition 490

Note:

Since, the tax base of the goodwill is nil, taxable temporary difference of Rs. 4,90,000 arises on goodwill.

However, no deferred tax is recognised on the goodwill. The deferred tax on other temporary differences arising

on acquisition is provided at 40% and not 30%, because taxes will be payable or recoverable in entity S’s tax

jurisdictions when the temporary differences will be reversed.

*Goodwill gives rise to a Permanent Difference.

2. 8