Page 24 - 3. COMPILER QB - INDAS 16

P. 24

SOLUTION

In accordance with Ind AS 16, all costs required to bring an asset to its present location and condition for its

intended use should be capitalised. Therefore, the initial purchase price of the building would be:

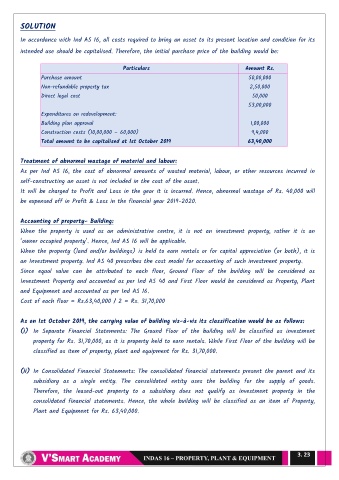

Particulars Amount Rs.

Purchase amount 50,00,000

Non-refundable property tax 2,50,000

Direct legal cost 50,000

53,00,000

Expenditures on redevelopment:

Building plan approval 1,00,000

Construction costs (10,00,000 – 60,000) 9,4,000

Total amount to be capitalised at 1st October 2019 63,40,000

Treatment of abnormal wastage of material and labour:

As per Ind AS 16, the cost of abnormal amounts of wasted material, labour, or other resources incurred in

self-constructing an asset is not included in the cost of the asset.

It will be charged to Profit and Loss in the year it is incurred. Hence, abnormal wastage of Rs. 40,000 will

be expensed off in Profit & Loss in the financial year 2019-2020.

Accounting of property- Building:

When the property is used as an administrative centre, it is not an investment property, rather it is an

―owner occupied property‖. Hence, Ind AS 16 will be applicable.

When the property (land and/or buildings) is held to earn rentals or for capital appreciation (or both), it is

an Investment property. Ind AS 40 prescribes the cost model for accounting of such investment property.

Since equal value can be attributed to each floor, Ground Floor of the building will be considered as

Investment Property and accounted as per Ind AS 40 and First Floor would be considered as Property, Plant

and Equipment and accounted as per Ind AS 16.

Cost of each floor = Rs.63,40,000 / 2 = Rs. 31,70,000

As on 1st October 2019, the carrying value of building vis-à-vis its classification would be as follows:

(i) In Separate Financial Statements: The Ground Floor of the building will be classified as investment

property for Rs. 31,70,000, as it is property held to earn rentals. While First Floor of the building will be

classified as item of property, plant and equipment for Rs. 31,70,000.

(ii) In Consolidated Financial Statements: The consolidated financial statements present the parent and its

subsidiary as a single entity. The consolidated entity uses the building for the supply of goods.

Therefore, the leased-out property to a subsidiary does not qualify as investment property in the

consolidated financial statements. Hence, the whole building will be classified as an item of Property,

Plant and Equipment for Rs. 63,40,000.

3. 23