Page 20 - 3. COMPILER QB - INDAS 16

P. 20

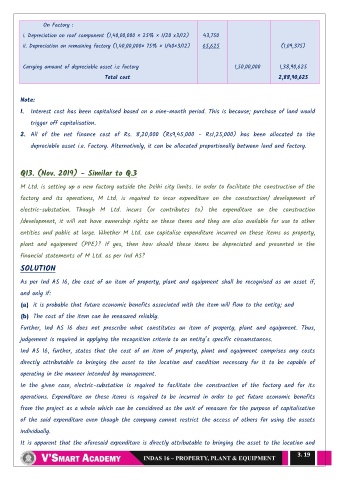

On Factory :

i. Depreciation on roof component (1,40,00,000 × 25% × 1/20 x3/12) 43,750

ii. Depreciation on remaining factory (1,40,00,000× 75% × 1/40×3/12) 65,625 (1,09,375)

Carrying amount of depreciable asset i.e factory 1,50,00,000 1,38,90,625

Total cost 2,88,90,625

Note:

1. Interest cost has been capitalised based on a nine-month period. This is because; purchase of land would

trigger off capitalisation.

2. All of the net finance cost of Rs. 8,20,000 (Rs9,45,000 - Rs1,25,000) has been allocated to the

depreciable asset i.e. Factory. Alternatively, it can be allocated proportionally between land and factory.

Q13. (Nov. 2019) - Similar to Q.3

M Ltd. is setting up a new factory outside the Delhi city limits. In order to facilitate the construction of the

factory and its operations, M Ltd. is required to incur expenditure on the construction/ development of

electric-substation. Though M Ltd. incurs (or contributes to) the expenditure on the construction

/development, it will not have ownership rights on these items and they are also available for use to other

entities and public at large. Whether M Ltd. can capitalise expenditure incurred on these items as property,

plant and equipment (PPE)? If yes, then how should these items be depreciated and presented in the

financial statements of M Ltd. as per Ind AS?

SOLUTION

As per Ind AS 16, the cost of an item of property, plant and equipment shall be recognised as an asset if,

and only if:

(a) it is probable that future economic benefits associated with the item will flow to the entity; and

(b) The cost of the item can be measured reliably.

Further, Ind AS 16 does not prescribe what constitutes an item of property, plant and equipment. Thus,

judgement is required in applying the recognition criteria to an entity‖s specific circumstances.

Ind AS 16, further, states that the cost of an item of property, plant and equipment comprises any costs

directly attributable to bringing the asset to the location and condition necessary for it to be capable of

operating in the manner intended by management.

In the given case, electric-substation is required to facilitate the construction of the factory and for its

operations. Expenditure on these items is required to be incurred in order to get future economic benefits

from the project as a whole which can be considered as the unit of measure for the purpose of capitalisation

of the said expenditure even though the company cannot restrict the access of others for using the assets

individually.

It is apparent that the aforesaid expenditure is directly attributable to bringing the asset to the location and

3. 19