Page 19 - 3. COMPILER QB - INDAS 16

P. 19

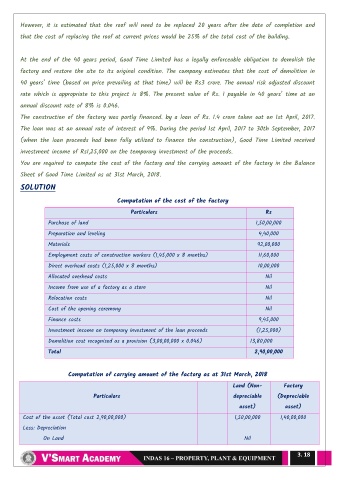

However, it is estimated that the roof will need to be replaced 20 years after the date of completion and

that the cost of replacing the roof at current prices would be 25% of the total cost of the building.

At the end of the 40 years period, Good Time Limited has a legally enforceable obligation to demolish the

factory and restore the site to its original condition. The company estimates that the cost of demolition in

40 years‖ time (based on price prevailing at that time) will be Rs3 crore. The annual risk adjusted discount

rate which is appropriate to this project is 8%. The present value of Rs. 1 payable in 40 years‖ time at an

annual discount rate of 8% is 0.046.

The construction of the factory was partly financed. by a loan of Rs. 1.4 crore taken out on 1st April, 2017.

The loan was at an annual rate of interest of 9%. During the period 1st April, 2017 to 30th September, 2017

(when the loan proceeds had been fully utilized to finance the construction), Good Time Limited received

investment income of Rs1,25,000 on the temporary investment of the proceeds.

You are required to compute the cost of the factory and the carrying amount of the factory in the Balance

Sheet of Good Time Limited as at 31st March, 2018.

SOLUTION

Computation of the cost of the factory

Particulars Rs

Purchase of land 1,50,00,000

Preparation and leveling 4,40,000

Materials 92,00,000

Employment costs of construction workers (1,45,000 x 8 months) 11,60,000

Direct overhead costs (1,25,000 x 8 months) 10,00,000

Allocated overhead costs Nil

Income from use of a factory as a store Nil

Relocation costs Nil

Cost of the opening ceremony Nil

Finance costs 9,45,000

Investment income on temporary investment of the loan proceeds (1,25,000)

Demolition cost recognised as a provision (3,00,00,000 x 0.046) 13,80,000

Total 2,90,00,000

Computation of carrying amount of the factory as at 31st March, 2018

Land (Non- Factory

Particulars depreciable (Depreciable

asset) asset)

Cost of the asset (Total cost 2,90,00,000) 1,50,00,000 1,40,00,000

Less: Depreciation

On Land Nil

3. 18