Page 22 - 3. COMPILER QB - INDAS 16

P. 22

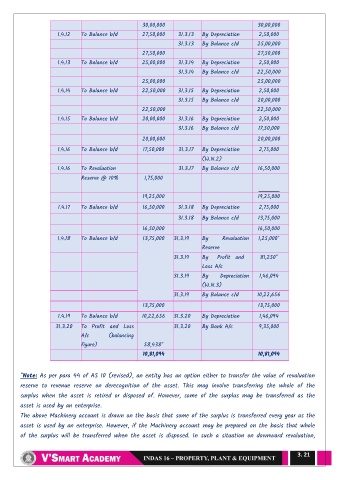

30,00,000 30,00,000

1.4.12 To Balance b/d 27,50,000 31.3.13 By Depreciation 2,50,000

31.3.13 By Balance c/d 25,00,000

27,50,000 27,50,000

1.4.13 To Balance b/d 25,00,000 31.3.14 By Depreciation 2,50,000

31.3.14 By Balance c/d 22,50,000

25,00,000 25,00,000

1.4.14 To Balance b/d 22,50,000 31.3.15 By Depreciation 2,50,000

31.3.15 By Balance c/d 20,00,000

22,50,000 22,50,000

1.4.15 To Balance b/d 20,00,000 31.3.16 By Depreciation 2,50,000

31.3.16 By Balance c/d 17,50,000

20,00,000 20,00,000

1.4.16 To Balance b/d 17,50,000 31.3.17 By Depreciation 2,75,000

(W.N.2)

1.4.16 To Revaluation 31.3.17 By Balance c/d 16,50,000

Reserve @ 10% 1,75,000

19,25,000 19,25,000

1.4.17 To Balance b/d 16,50,000 31.3.18 By Depreciation 2,75,000

31.3.18 By Balance c/d 13,75,000

16,50,000 16,50,000

1.4.18 To Balance b/d 13,75,000 31.3.19 By Revaluation 1,25,000*

Reserve

31.3.19 By Profit and 81,250*

Loss A/c

31.3.19 By Depreciation 1,46,094

(W.N.3)

31.3.19 By Balance c/d 10,22,656

13,75,000 13,75,000

1.4.19 To Balance b/d 10,22,656 31.3.20 By Depreciation 1,46,094

31.3.20 To Profit and Loss 31.3.20 By Bank A/c 9,35,000

A/c (balancing

figure) 58,438*

10,81,094 10,81,094

*Note: As per para 44 of AS 10 (revised), an entity has an option either to transfer the value of revaluation

reserve to revenue reserve on derecognition of the asset. This may involve transferring the whole of the

surplus when the asset is retired or disposed of. However, some of the surplus may be transferred as the

asset is used by an enterprise.

The above Machinery account is drawn on the basis that some of the surplus is transferred every year as the

asset is used by an enterprise. However, if the Machinery account may be prepared on the basis that whole

of the surplus will be transferred when the asset is disposed. In such a situation on downward revaluation,

3. 21