Page 9 - 4. COMPILER QB - INDAS 38

P. 9

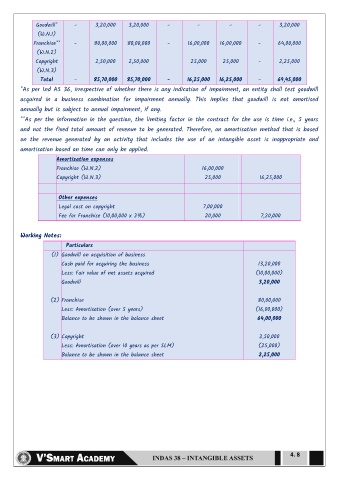

Goodwill* - 3,20,000 3,20,000 - - - - 3,20,000

(W.N.1)

Franchise** - 80,00,000 80,00,000 - 16,00,000 16,00,000 - 64,00,000

(W.N.2)

Copyright 2,50,000 2,50,000 25,000 25,000 - 2,25,000

(W.N.3)

Total - 85,70,000 85,70,000 - 16,25,000 16,25,000 - 69,45,000

*As per Ind AS 36, irrespective of whether there is any indication of impairment, an entity shall test goodwill

acquired in a business combination for impairment annually. This implies that goodwill is not amortised

annually but is subject to annual impairment, if any.

**As per the information in the question, the limiting factor in the contract for the use is time i.e., 5 years

and not the fixed total amount of revenue to be generated. Therefore, an amortisation method that is based

on the revenue generated by an activity that includes the use of an intangible asset is inappropriate and

amortisation based on time can only be applied.

2. Amortization expenses

Franchise (W.N.2) 16,00,000

3. Copyright (W.N.3) 25,000 16,25,000

Other expenses

Legal cost on copyright 7,00,000

Fee for Franchise (10,00,000 x 2%) 20,000 7,20,000

Working Notes:

P Particulars Rs.

(1) Goodwill on acquisition of business

Cash paid for acquiring the business 13,20,000

Less: Fair value of net assets acquired (10,00,000)

Goodwill 3,20,000

(2) Franchise 80,00,000

Less: Amortisation (over 5 years) (16,00,000)

Balance to be shown in the balance sheet 64,00,000

(3) Copyright 2,50,000

Less: Amortisation (over 10 years as per SLM) (25,000)

Balance to be shown in the balance sheet 2,25,000

4. 8