Page 7 - 4. COMPILER QB - INDAS 38

P. 7

QUESTIONS FROM PAST EXAM PAPERS

Q7 (May 19)

CARP Ltd. is engaged in developing computer software. The expenditures incurred by CARP Ltd. in pursuance

of its development of software is given below:

(i) Paid Rs. 1,50,000 towards salaries of the program designers.

(ii) Incurred Rs. 3,00,000 towards other costs of completion of program design.

(iii) Incurred Rs.80,000 towards cost of coding and establishing technical feasibility.

(iv) Paid Rs. 3,00,000 for other direct costs after establishment of technical feasibility.

(v) Incurred Rs. 90,000 towards other testing costs.

(vi) A focus group of other software developers was invited to a conference for the introduction of this new

software. Cost of the conference aggregated to Rs.60,000.

(vii) On March 15, 2018, the development phase was completed and a cash flow budget was prepared.

Net profit for the year 2017-18 was estimated to be equal Rs. 30,00,000.

How should CARP Ltd. account for the above-mentioned cost as per relevant Ind AS?

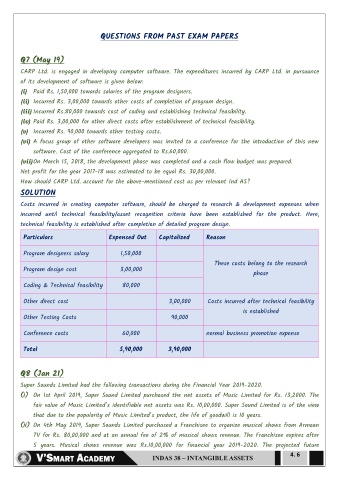

SOLUTION

Costs incurred in creating computer software, should be charged to research & development expenses when

incurred until technical feasibility/asset recognition criteria have been established for the product. Here,

technical feasibility is established after completion of detailed program design.

Particulars Expensed Out Capitalized Reason

Program designers salary 1,50,000

These costs belong to the research

Program design cost 3,00,000

phase

Coding & Technical feasibility 80,000

Other direct cost 3,00,000 Costs incurred after technical feasibility

is established

Other Testing Costs 90,000

Conference costs 60,000 normal business promotion expense

Total 5,90,000 3,90,000

Q8 (Jan 21)

Super Sounds Limited had the following transactions during the Financial Year 2019-2020.

(i) On 1st April 2019, Super Sound Limited purchased the net assets of Music Limited for Rs. 13,2000. The

fair value of Music Limited’s identifiable net assets was Rs. 10,00,000. Super Sound Limited is of the view

that due to the popularity of Music Limited’s product, the life of goodwill is 10 years.

(ii) On 4th May 2019, Super Sounds Limited purchased a Franchisee to organize musical shows from Armaan

TV for Rs. 80,00,000 and at an annual fee of 2% of musical shows revenue. The Franchisee expires after

5 years. Musical shows revenue was Rs.10,00,000 for financial year 2019-2020. The projected future

4. 6