Page 10 - 6. COMPILER QB - INDAS 116

P. 10

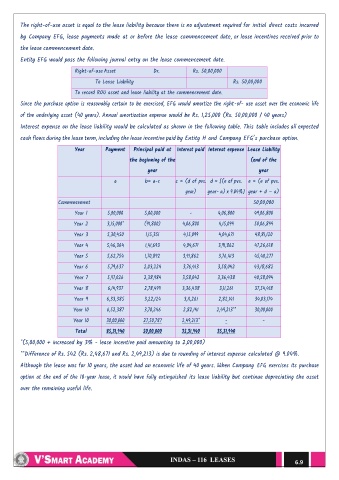

The right-of-use asset is equal to the lease liability because there is no adjustment required for initial direct costs incurred

by Company EFG, lease payments made at or before the lease commencement date, or lease incentives received prior to

the lease commencement date.

Entity EFG would pass the following journal entry on the lease commencement date.

Right-of-use Asset Dr. Rs. 50,00,000

To Lease Liability Rs. 50,00,000

To record ROU asset and lease liability at the commencement date.

Since the purchase option is reasonably certain to be exercised, EFG would amortize the right-of- use asset over the economic life

of the underlying asset (40 years). Annual amortization expense would be Rs. 1,25,000 (Rs. 50,00,000 / 40 years)

Interest expense on the lease liability would be calculated as shown in the following table. This table includes all expected

cash flows during the lease term, including the lease incentive paid by Entity H and Company EFG’s purchase option.

Year Payment Principal paid at Interest paid Interest expense Lease Liability

the beginning of the (end of the

year year

a b= a-c c = (d of pvs. d = [(e of pvs. e = (e of pvs.

year) year- a) x 9.04%] year + d – a)

Commencement 50,00,000

Year 1 5,00,000 5,00,000 - 4,06,800 49,06,800

Year 2 3,15,000* (91,800) 4,06,800 4,15,099 50,06,899

Year 3 5,30,450 1,15,351 4,15,099 4,04,671 48,81,120

Year 4 5,46,364 1,41,693 4,04,671 3,91,862 47,26,618

Year 5 5,62,754 1,70,892 3,91,862 3,76,413 45,40,277

Year 6 5,79,637 2,03,224 3,76,413 3,58,042 43,18,682

Year 7 5,97,026 2,38,984 3,58,042 3,36,438 40,58,094

Year 8 6,14,937 2,78,499 3,36,438 3,11,261 37,54,418

Year 9 6,33,385 3,22,124 3,11,261 2,82,141 34,03,174

Year 10 6,52,387 3,70,246 2,82,141 2,49,213** 30,00,000

Year 10 30,00,000 27,50,787 2,49,213* - -

Total 85,31,940 50,00,000 35,31,940 35,31,940

*(5,00,000 + increased by 3% - lease incentive paid amounting to 2,00,000)

**Difference of Rs. 542 (Rs. 2,48,671 and Rs. 2,49,213) is due to rounding of interest expense calculated @ 9.04%.

Although the lease was for 10 years, the asset had an economic life of 40 years. When Company EFG exercises its purchase

option at the end of the 10-year lease, it would have fully extinguished its lease liability but continue depreciating the asset

over the remaining useful life.

6.9