Page 11 - 8. COMPILER QB - INDAS 41

P. 11

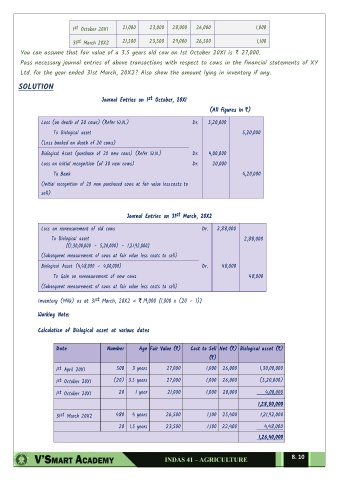

1 st October 20X1 21,000 23,000 28,000 26,000 1,000

31 st March 20X2 21,500 23,500 29,000 26,500 1,100

You can assume that fair value of a 3.5 years old cow on 1st October 20X1 is ` 27,000.

Pass necessary journal entries of above transactions with respect to cows in the financial statements of XY

Ltd. for the year ended 31st March, 20X2? Also show the amount lying in inventory if any.

SOLUTION

Journal Entries on 1 st October, 20X1

(All figures in `)

Loss (on death of 20 cows) (Refer W.N.) Dr. 5,20,000

To Biological asset 5,20,000

(Loss booked on death of 20 cows)

Biological Asset (purchase of 20 new cows) (Refer W.N.) Dr. 4,00,000

Loss on initial recognition (of 20 new cows) Dr. 20,000

To Bank 4,20,000

(Initial recognition of 20 new purchased cows at fair value less costs to

sell)

Journal Entries on 31 st March, 20X2

Loss on remeasurement of old cows Dr. 2,88,000

To Biological asset 2,88,000

[(1,30,00,000 – 5,20,000) – 1,21,92,000]

(Subsequent measurement of cows at fair value less costs to sell)

Biological Asset (4,48,000 – 4,00,000) Dr. 48,000

To Gain on remeasurement of new cows 48,000

(Subsequent measurement of cows at fair value less costs to sell)

Inventory (Milk) as at 31 st March, 20X2 = ` 19,000 [1,000 x (20 – 1)]

Working Note:

Calculation of Biological asset at various dates

Date Number Age Fair Value (`) Cost to Sell Net (`) Biological asset (`)

(`)

1 st April 20X1 500 3 years 27,000 1,000 26,000 1,30,00,000

1 st October 20X1 (20) 3.5 years 27,000 1,000 26,000 (5,20,000)

1 st October 20X1 20 1 year 21,000 1,000 20,000 4,00,000

1,28,80,000

31 st March 20X2 480 4 years 26,500 1,100 25,400 1,21,92,000

20 1.5 years 23,500 1,100 22,400 4,48,000

1,26,40,000

8. 10