Page 19 - 16. COMPILER QB - INDAS 103

P. 19

To be capable of being conducted and managed for the purpose identified in the definition of a business,

an integrated set of activities and assets requires two essential elements—inputs and processes applied to

those inputs.

Therefore, an integrated set of activities and assets must include, at a minimum, an input and a

substantive process that together significantly contribute to the ability to create output.

In the aforesaid transaction, Company X acquired share of participating rights owned by Company Z for

the producing Block (AWM/01). The output in this transaction (Considering AWM/01) is a producing block.

Also all the manpower and requisite facilities / machineries are owned by Joint venture and thereby all

the Joint Operators. Hence, acquiring participating rights amounts to acquiring inputs (Expertise Manpower

& Machinery) and it is critical to the ability to continue producing outputs. Thus, the said acquisition will

fall under the Business Acquisition and hence standard Ind AS 103 is to be applied for the same.

(2) As per Ind AS 103, acquisition date is the date on which the acquirer obtains control of the acquiree.

Further, Ind AS 103 clarifies that the date on which the acquirer obtains control of the acquiree is

generally the date on which the acquirer legally transfers the consideration, acquires the assets and

assumes the liabilities of the acquiree at the closing date. However, the acquirer might obtain control on a

date that is either earlier or later than the closing date.

An acquirer shall consider all pertinent facts and circumstances in identifying the acquisition date. Since

government of India (GOI) approval is a substantive approval for Company X to acquire control of

Company Z‖s operations, the date of acquisition cannot be earlier than the date on which approval is

obtained from GOI. This is pertinent given that the approval from GOI is considered to be a substantive

process and accordingly, the acquisition is considered to be completed only on receipt of such approval.

Hence acquisition date in the above scenario is 30 6.20X1.

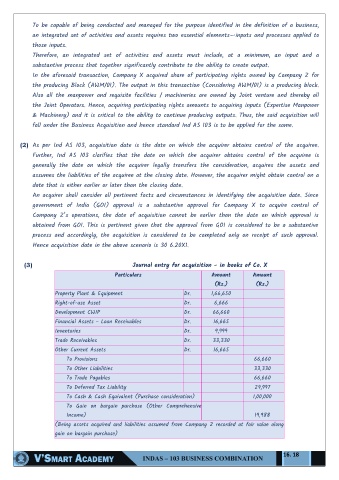

(3) Journal entry for acquisition - in books of Co. X

Particulars Amount Amount

(Rs.) (Rs.)

Property Plant & Equipment Dr. 1,66,650

Right-of-use Asset Dr. 6,666

Development CWIP Dr. 66,660

Financial Assets - Loan Receivables Dr. 16,665

Inventories Dr. 9,999

Trade Receivables Dr. 33,330

Other Current Assets Dr. 16,665

To Provisions 66,660

To Other Liabilities 33,330

To Trade Payables 66,660

To Deferred Tax Liability 29,997

To Cash & Cash Equivalent (Purchase consideration) 1,00,000

To Gain on bargain purchase (Other Comprehensive

Income) 19,988

(Being assets acquired and liabilities assumed from Company Z recorded at fair value along

gain on bargain purchase)

16. 18