Page 59 - 16. COMPILER QB - INDAS 103

P. 59

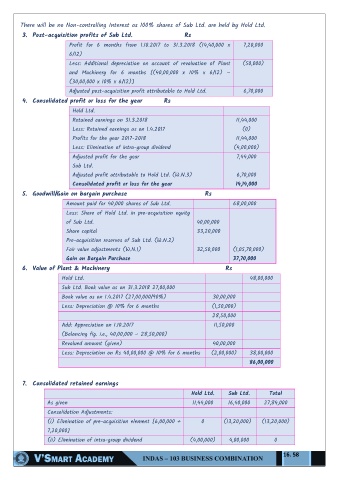

There will be no Non-controlling Interest as 100% shares of Sub Ltd. are held by Hold Ltd.

3. Post-acquisition profits of Sub Ltd. Rs

Profit for 6 months from 1.10.2017 to 31.3.2018 (14,40,000 x 7,20,000

6/12)

Less: Additional depreciation on account of revaluation of Plant (50,000)

and Machinery for 6 months [(40,00,000 x 10% x 6/12) –

(30,00,000 x 10% x 6/12)]

Adjusted post-acquisition profit attributable to Hold Ltd. 6,70,000

4. Consolidated profit or loss for the year Rs

Hold Ltd.

Retained earnings on 31.3.2018 11,44,000

Less: Retained earnings as on 1.4.2017 (0)

Profits for the year 2017-2018 11,44,000

Less: Elimination of intra-group dividend (4,00,000)

Adjusted profit for the year 7,44,000

Sub Ltd.

Adjusted profit attributable to Hold Ltd. (W.N.3) 6,70,000

Consolidated profit or loss for the year 14,14,000

5. Goodwill/Gain on bargain purchase Rs

Amount paid for 40,000 shares of Sub Ltd. 68,00,000

Less: Share of Hold Ltd. in pre-acquisition equity

of Sub Ltd. 40,00,000

Share capital 33,20,000

Pre-acquisition reserves of Sub Ltd. (W.N.2)

Fair value adjustments (W.N.1) 32,50,000 (1,05,70,000)

Gain on Bargain Purchase 37,70,000

6. Value of Plant & Machinery Rs

Hold Ltd. 48,00,000

Sub Ltd. Book value as on 31.3.2018 27,00,000

Book value as on 1.4.2017 (27,00,000/90%) 30,00,000

Less: Depreciation @ 10% for 6 months (1,50,000)

28,50,000

Add: Appreciation on 1.10.2017 11,50,000

(Balancing fig. i.e., 40,00,000 – 28,50,000)

Revalued amount (given) 40,00,000

Less: Depreciation on Rs 40,00,000 @ 10% for 6 months (2,00,000) 38,00,000

86,00,000

7. Consolidated retained earnings

Hold Ltd. Sub Ltd. Total

As given 11,44,000 16,40,000 27,84,000

Consolidation Adjustments:

(i) Elimination of pre-acquisition element [6,00,000 + 0 (13,20,000) (13,20,000)

7,20,000]

(ii) Elimination of intra-group dividend (4,00,000) 4,00,000 0

16. 58