Page 65 - 16. COMPILER QB - INDAS 103

P. 65

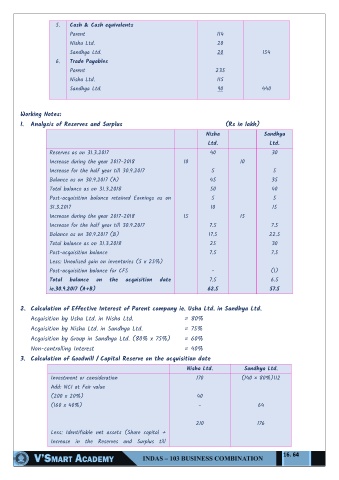

5. Cash & Cash equivalents

Parent 114

Nisha Ltd. 20

Sandhya Ltd. 20 154

6. Trade Payables

Parent 235

Nisha Ltd. 115

Sandhya Ltd. 90 440

Working Notes:

1. Analysis of Reserves and Surplus (Rs in lakh)

Nisha Sandhya

Ltd. Ltd.

Reserves as on 31.3.2017 40 30

Increase during the year 2017-2018 10 10

Increase for the half year till 30.9.2017 5 5

Balance as on 30.9.2017 (A) 45 35

Total balance as on 31.3.2018 50 40

Post-acquisition balance retained Earnings as on 5 5

31.3.2017 10 15

Increase during the year 2017-2018 15 15

Increase for the half year till 30.9.2017 7.5 7.5

Balance as on 30.9.2017 (B) 17.5 22.5

Total balance as on 31.3.2018 25 30

Post-acquisition balance 7.5 7.5

Less: Unealised gain on inventories (5 x 25%)

Post-acquisition balance for CFS - (1)

Total balance on the acquisition date 7.5 6.5

ie.30.9.2017 (A+B) 62.5 57.5

2. Calculation of Effective Interest of Parent company ie. Usha Ltd. in Sandhya Ltd.

Acquisition by Usha Ltd. in Nisha Ltd. = 80%

Acquisition by Nisha Ltd. in Sandhya Ltd. = 75%

Acquisition by Group in Sandhya Ltd. (80% x 75%) = 60%

Non-controlling Interest = 40%

3. Calculation of Goodwill / Capital Reserve on the acquisition date

Nisha Ltd. Sandhya Ltd.

Investment or consideration 170 (140 × 80%)112

Add: NCI at Fair value

(200 x 20%) 40

(160 x 40%) - 64

210 176

Less: Identifiable net assets (Share capital +

Increase in the Reserves and Surplus till

16. 64