Page 68 - 16. COMPILER QB - INDAS 103

P. 68

earned Rs 20 lakh profit in the preceding year and expects to earn another Rs 10 lakh.

(3) In addition to above, David Ltd. also has agreed to pay one of the founder shareholder-Director a

payment of Rs 25 lakh provided he stays with the Company for two years after the acquisition.

(4) Parker Ltd. had certain equity settled share-based payment award (original award) which got

replaced by the new awards issued by David Ltd. As per the original term, the vesting period was 4

years and as of the acquisition date the employees of Parker Ltd. have already served 2 years of

service. As per the replaced awards, the vesting period has been reduced to one year (one year from

the acquisition date). The fair value of the award on the acquisition date was as follows:

Original award - Rs 6 lakh Replacement award - Rs 9 lakh

(5) Parker Ltd. had a lawsuit pending with a customer who had made a claim of Rs 35 lakh.

Management reliably estimated the fair value of the liability to be Rs 10 lakh.

(6) The applicable tax rate for both entities is 40%.

st

You are required to prepare opening consolidated balance sheet of David Ltd. as on 1 April, 2019 along with

workings. Assume discount rate of 8%.

SOLUTION

st

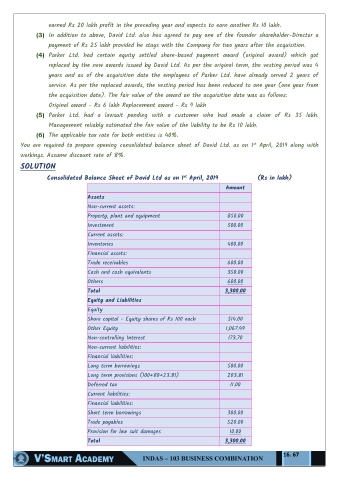

Consolidated Balance Sheet of David Ltd as on 1 April, 2019 (Rs in lakh)

Amount

Assets

Non-current assets:

Property, plant and equipment 850.00

Investment 500.00

Current assets:

Inventories 400.00

Financial assets:

Trade receivables 600.00

Cash and cash equivalents 350.00

Others 600.00

Total 3,300.00

Equity and Liabilities

Equity

Share capital - Equity shares of Rs 100 each 514.00

Other Equity 1,067.49

Non-controlling Interest 173.70

Non-current liabilities:

Financial liabilities:

Long term borrowings 500.00

Long term provisions (100+80+23.81) 203.81

Deferred tax 11.00

Current liabilities:

Financial liabilities:

Short term borrowings 300.00

Trade payables 520.00

Provision for law suit damages 10.00

Total 3,300.00

16. 67