Page 73 - 16. COMPILER QB - INDAS 103

P. 73

financial statements of Group A immediately before the merger would now be a part of the separate financial

statements of A Ltd. Accordingly, it would be appropriate to recognise the carrying value of the assets,

liabilities and reserves pertaining to B Ltd as appearing in the consolidated financial statements of A Ltd.

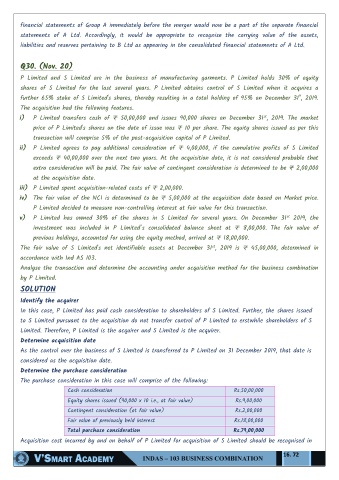

Q30. (Nov. 20)

P Limited and S Limited are in the business of manufacturing garments. P Limited holds 30% of equity

shares of S Limited for the last several years. P Limited obtains control of S Limited when it acquires a

further 65% stake of S Limited's shares, thereby resulting in a total holding of 95% on December 31", 2019.

The acquisition had the following features.

i) P Limited transfers cash of ₹ 50,00,000 and issues 90,000 shares on December 31 , 2019. The market

st

price of P Limited's shares on the date of issue was ₹ 10 per share. The equity shares issued as per this

transaction will comprise 5% of the post-acquisition capital of P Limited.

ii) P Limited agrees to pay additional consideration of ₹ 4,00,000, if the cumulative profits of S Limited

exceeds ₹ 40,00,000 over the next two years. At the acquisition date, it is not considered probable that

extra consideration will be paid. The fair value of contingent consideration is determined to be ₹ 2,00,000

at the acquisition date.

iii) P Limited spent acquisition-related costs of ₹ 2,00,000.

iv) The fair value of the NCI is determined to be ₹ 5,00,000 at the acquisition date based on Market price.

P Limited decided to measure non-controlling interest at fair value for this transaction.

st

v) P Limited has owned 30% of the shares in S Limited for several years. On December 31 2019, the

investment was included in P Limited‖s consolidated balance sheet at ₹ 8,00,000. The fair value of

previous holdings, accounted for using the equity method, arrived at ₹ 18,00,000.

st

The fair value of S Limited's net identifiable assets at December 31 , 2019 is ₹ 45,00,000, determined in

accordance with Ind AS 103.

Analyse the transaction and determine the accounting under acquisition method for the business combination

by P Limited.

SOLUTION

Identify the acquirer

In this case, P Limited has paid cash consideration to shareholders of S Limited. Further, the shares issued

to S Limited pursuant to the acquisition do not transfer control of P Limited to erstwhile shareholders of S

Limited. Therefore, P Limited is the acquirer and S Limited is the acquirer.

Determine acquisition date

As the control over the business of S Limited is transferred to P Limited on 31 December 2019, that date is

considered as the acquisition date.

Determine the purchase consideration

The purchase consideration in this case will comprise of the following:

Cash consideration ₨.50,00,000

Equity shares issued (90,000 x 10 i.e., at fair value) ₨.9,00,000

Contingent consideration (at fair value) ₨.2,00,000

Fair value of previously held interest ₨.18,00,000

Total purchase consideration ₨.79,00,000

Acquisition cost incurred by and on behalf of P Limited for acquisition of S Limited should be recognised in

16. 72