Page 85 - 16. COMPILER QB - INDAS 103

P. 85

Rs in '000

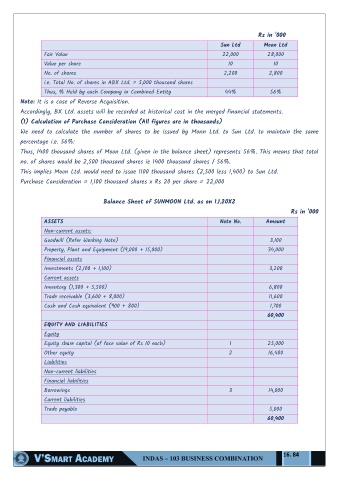

Sun Ltd Moon Ltd

Fair Value 22,000 28,000

Value per share 10 10

No. of shares 2,200 2,800

i.e. Total No. of shares in ABX Ltd. = 5,000 thousand shares

Thus, % Held by each Company in Combined Entity 44% 56%

Note: It is a case of Reverse Acquisition.

Accordingly, BX Ltd. assets will be recorded at historical cost in the merged financial statements.

(1) Calculation of Purchase Consideration (All figures are in thousands)

We need to calculate the number of shares to be issued by Monn Ltd. to Sun Ltd. to maintain the same

percentage i.e. 56%:

Thus, 1400 thousand shares of Moon Ltd. (given in the balance sheet) represents 56%. This means that total

no. of shares would be 2,500 thousand shares ie 1400 thousand shares / 56%.

This implies Moon Ltd. would need to issue 1100 thousand shares (2,500 less 1,400) to Sun Ltd.

Purchase Consideration = 1,100 thousand shares x Rs 20 per share = 22,000

Balance Sheet of SUNMOON Ltd. as on 1.1.20X2

Rs in '000

ASSETS Note No. Amount

Non-current assets:

Goodwill (Refer Working Note) 3,100

Property, Plant and Equipment (19,000 + 15,000) 34,000

Financial assets

Investments (2,100 + 1,100) 3,200

Current assets

Inventory (1,300 + 5,500) 6,800

Trade receivable (3,600 + 8,000) 11,600

Cash and Cash equivalent (900 + 800) 1,700

60,400

EQUITY AND LIABILITIES

Equity

Equity share capital (of face value of Rs 10 each) 1 25,000

Other equity 2 16,400

Liabilities

Non-current liabilities

Financial liabilities

Borrowings 3 14,000

Current liabilities

Trade payable 5,000

60,400

16. 84