Page 83 - 16. COMPILER QB - INDAS 103

P. 83

The fair value of net assets of SUN and MOON limited are as follows:

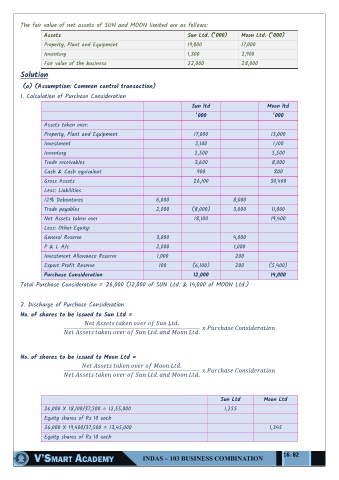

Assets Sun Ltd. (‘000) Moon Ltd. (‘000)

Property, Plant and Equipment 19,000 17,000

Inventory 1,300 2,900

Fair value of the business 22,000 28,000

Solution

(a) (Assumption: Common control transaction)

1. Calculation of Purchase Consideration

Sun ltd Moon ltd

‘000 ‘000

Assets taken over:

Property, Plant and Equipment 17,000 15,000

Investment 2,100 1,100

Inventory 2,500 5,500

Trade receivables 3,600 8,000

Cash & Cash equivalent 900 800

Gross Assets 26,100 30,400

Less: Liabilities

12% Debentures 6,000 8,000

Trade payables 2,000 (8,000) 3,000 11,000

Net Assets taken over 18,100 19,400

Less: Other Equity:

General Reserve 3,000 4,000

P & L A/c 2,000 1,000

Investment Allowance Reserve 1,000 200

Export Profit Reserve 100 (6,100) 200 (5,400)

Purchase Consideration 12,000 14,000

Total Purchase Consideration = 26,000 (12,000 of SUN Ltd. & 14,000 of MOON Ltd.)

2. Discharge of Purchase Consideration

No. of shares to be issued to Sun Ltd =

.

ℎ

. .

No. of shares to be issued to Moon Ltd =

.

ℎ

. .

Sun Ltd Moon Ltd

26,000 X 18,100/37,500 = 12,55,000 1,255

Equity shares of Rs 10 each

26,000 X 19,400/37,500 = 13,45,000 1,345

Equity shares of Rs 10 each

16. 82