Page 84 - 16. COMPILER QB - INDAS 103

P. 84

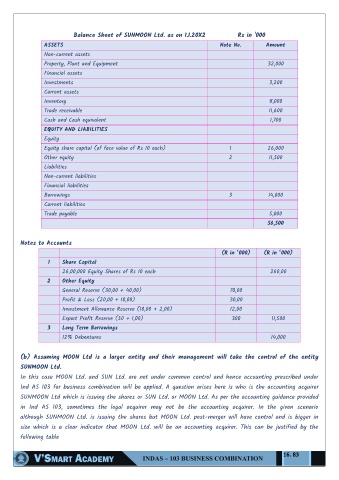

Balance Sheet of SUNMOON Ltd. as on 1.1.20X2 Rs in '000

ASSETS Note No. Amount

Non-current assets

Property, Plant and Equipment 32,000

Financial assets

Investments 3,200

Current assets

Inventory 8,000

Trade receivable 11,600

Cash and Cash equivalent 1,700

EQUITY AND LIABILITIES

Equity

Equity share capital (of face value of Rs 10 each) 1 26,000

Other equity 2 11,500

Liabilities

Non-current liabilities

Financial liabilities

Borrowings 3 14,000

Current liabilities

Trade payable 5,000

56,500

Notes to Accounts

(R in ‘000) (R in ‘000)

1 Share Capital

26,00,000 Equity Shares of Rs 10 each 260,00

2 Other Equity

General Reserve (30,00 + 40,00) 70,00

Profit & Loss (20,00 + 10,00) 30,00

Investment Allowance Reserve (10,00 + 2,00) 12,00

Export Profit Reserve (50 + 1,00) 300 11,500

3 Long Term Borrowings

12% Debentures 14,000

(b) Assuming MOON Ltd is a larger entity and their management will take the control of the entity

SUNMOON Ltd.

In this case MOON Ltd. and SUN Ltd. are not under common control and hence accounting prescribed under

Ind AS 103 for business combination will be applied. A question arises here is who is the accounting acquirer

SUNMOON Ltd which is issuing the shares or SUN Ltd. or MOON Ltd. As per the accounting guidance provided

in Ind AS 103, sometimes the legal acquirer may not be the accounting acquirer. In the given scenario

although SUNMOON Ltd. is issuing the shares but MOON Ltd. post-merger will have control and is bigger in

size which is a clear indicator that MOON Ltd. will be an accounting acquirer. This can be justified by the

following table

16. 83