Page 81 - 16. COMPILER QB - INDAS 103

P. 81

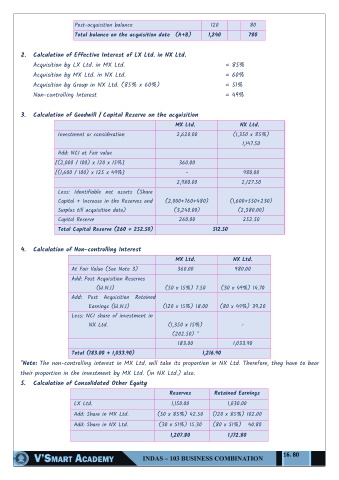

Post-acquisition balance 120 80

Total balance on the acquisition date (A+B) 1,240 780

2. Calculation of Effective Interest of LX Ltd. in NX Ltd.

Acquisition by LX Ltd. in MX Ltd. = 85%

Acquisition by MX Ltd. in NX Ltd. = 60%

Acquisition by Group in NX Ltd. (85% x 60%) = 51%

Non-controlling Interest = 49%

3. Calculation of Goodwill / Capital Reserve on the acquisition

MX Ltd. NX Ltd.

Investment or consideration 2,620.00 (1,350 x 85%)

1,147.50

Add: NCI at Fair value

[(2,000 / 100) x 120 x 15%] 360.00

[(1,600 / 100) x 125 x 49%] - 980.00

2,980.00 2,127.50

Less: Identifiable net assets (Share

Capital + Increase in the Reserves and (2,000+760+480) (1,600+550+230)

Surplus till acquisition date) (3,240.00) (2,380.00)

Capital Reserve 260.00 252.50

Total Capital Reserve (260 + 252.50) 512.50

4. Calculation of Non-controlling Interest

MX Ltd. NX Ltd.

At Fair Value (See Note 3) 360.00 980.00

Add: Post Acquisition Reserves

(W.N.1) (50 x 15%) 7.50 (30 x 49%) 14.70

Add: Post Acquisition Retained

Earnings (W.N.1) (120 x 15%) 18.00 (80 x 49%) 39.20

Less: NCI share of investment in

NX Ltd. (1,350 x 15%) -

(202.50) *

183.00 1,033.90

Total (183.00 + 1,033.90) 1,216.90

*Note: The non-controlling interest in MX Ltd. will take its proportion in NX Ltd. Therefore, they have to bear

their proportion in the investment by MX Ltd. (in NX Ltd.) also.

5. Calculation of Consolidated Other Equity

Reserves Retained Earnings

LX Ltd. 1,150.00 1,030.00

Add: Share in MX Ltd. (50 x 85%) 42.50 (120 x 85%) 102.00

Add: Share in NX Ltd. (30 x 51%) 15.30 (80 x 51%) 40.80

1,207.80 1,172.80

16. 80