Page 11 - 19. COMPILER QB - INDAS 115

P. 11

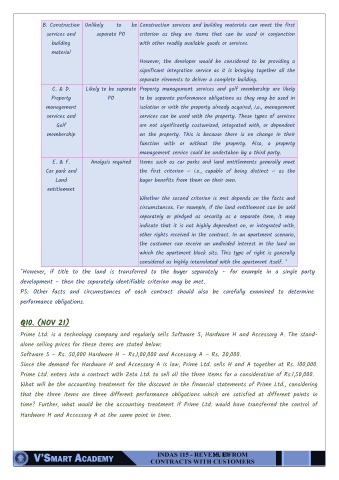

B. Construction Unlikely to be Construction services and building materials can meet the first

services and separate PO criterion as they are items that can be used in conjunction

building with other readily available goods or services.

material

However, the developer would be considered to be providing a

significant integration service as it is bringing together all the

separate elements to deliver a complete building.

C. & D. Likely to be separate Property management services and golf membership are likely

Property PO to be separate performance obligations as they may be used in

management isolation or with the property already acquired, i.e., management

services and services can be used with the property. These types of services

Golf are not significantly customized, integrated with, or dependent

membership on the property. This is because there is no change in their

function with or without the property. Also, a property

management service could be undertaken by a third party.

E. & F. Analysis required Items such as car parks and land entitlements generally meet

Car park and the first criterion – i.e., capable of being distinct – as the

Land buyer benefits from them on their own.

entitlement

Whether the second criterion is met depends on the facts and

circumstances. For example, if the land entitlement can be sold

separately or pledged as security as a separate item, it may

indicate that it is not highly dependent on, or integrated with,

other rights received in the contract. In an apartment scenario,

the customer can receive an undivided interest in the land on

which the apartment block sits. This type of right is generally

considered as highly interrelated with the apartment itself. *

*However, if title to the land is transferred to the buyer separately – for example in a single party

development – then the separately identifiable criterion may be met.

PS: Other facts and circumstances of each contract should also be carefully examined to determine

performance obligations.

Q10. (NOV 21)

Prime Ltd. is a technology company and regularly sells Software S, Hardware H and Accessory A. The stand-

alone selling prices for these items are stated below:

Software S – Rs. 50,000 Hardware H – Rs.1,00,000 and Accessory A – Rs. 20,000.

Since the demand for Hardware H and Accessory A is low, Prime Ltd. sells H and A together at Rs. 100,000.

Prime Ltd. enters into a contract with Zeta Ltd. to sell all the three items for a consideration of Rs.1,50,000.

What will be the accounting treatment for the discount in the financial statements of Prime Ltd., considering

that the three items are three different performance obligations which are satisfied at different points in

time? Further, what would be the accounting treatment if Prime Ltd. would have transferred the control of

Hardware H and Accessory A at the same point in time.

19. 10