Page 29 - 19. COMPILER QB - INDAS 115

P. 29

(ii) Calculate the amount of revenue which A Ltd. must allocate to each component of the transaction;

(iii) Prepare journal entries to record the information set out above in the books of accounts of A Ltd. for the

years ended 31st March·2019 and 31st March 2020; and

(iv) Draft an extract showing how revenue could be presented and disclosed in the financial statements of A

Ltd. for the year ended 31st March 2019 and 31st March 2020.

SOLUTION

i) As per Ind AS 115, a good or service that is promised to customer is distinct if both of the following

criteria are met:

a) The customer can benefit from the good or service either on its own or together with other resources that

are readily available to them. A readily available resource is a good or service that is sold separately (by

the entity or another entity) or that the customer has already obtained from the entity or from other

transactions or events; and

b) The entity‖s promise to transfer the goods or service to the customer is separately identifiable from other

promises in the contract.

Factors that indicate two or more promise to transfer goods or services to a customer are separately

identifiable include, but are not limited to, the following:

a) Significant integration services are not provided (i.e. the entity is not using the goods or services as

inputs to produce or deliver the combined output called for in the contract)

b) The goods or services do not significantly modify or customize other promised goods or services in the

contract.

c) The goods or services are not highly inter–dependent or highly interrelated with other promised goods

or services in the contract.

Accordingly, on 1st April, 2018, entity A entered into a single transaction with three identifiable separate

components:

1. Sale of goods (i.e. engineering machine);

2. Rendering of services (i.e. engineering machine maintenance service on 30th September, 2018 and 1st

April, 2019); and

3. Providing finance (i.e. sale of engineering machine and rendering of services on extended period credit)

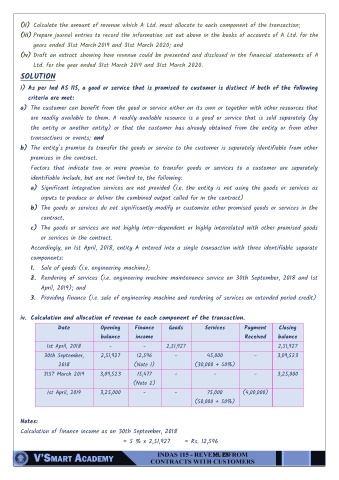

iv. Calculation and allocation of revenue to each component of the transaction.

Date Opening Finance Goods Services Payment Closing

balance income Received balance

1st April, 2018 - - 2,51,927 2,51,927

30th September, 2,51,927 12,596 - 45,000 - 3,09,523

2018 (Note 1) (30,000 + 50%)

31ST March 2019 3,09,523 15,477 - - - 3,25,000

(Note 2)

1st April, 2019 3,25,000 - - 75,000 (4,00,000)

(50,000 + 50%)

Notes:

Calculation of finance income as on 30th September, 2018

= 5 % x 2,51,927 = Rs. 12,596

19. 28