Page 3 - 23. COMPILER QB - IND AS 109_32

P. 3

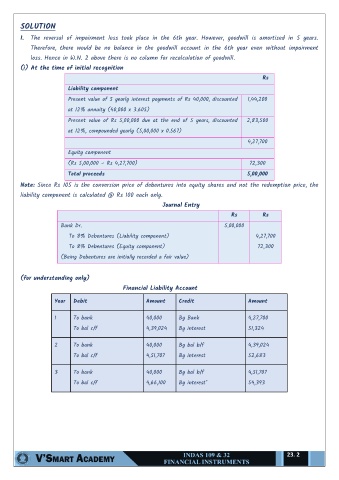

SOLUTION

1. The reversal of impairment loss took place in the 6th year. However, goodwill is amortised in 5 years.

Therefore, there would be no balance in the goodwill account in the 6th year even without impairment

loss. Hence in W.N. 2 above there is no column for recalculation of goodwill.

(i) At the time of initial recognition

Rs

Liability component

Present value of 5 yearly interest payments of Rs 40,000, discounted 1,44,200

at 12% annuity (40,000 x 3.605)

Present value of Rs 5,00,000 due at the end of 5 years, discounted 2,83,500

at 12%, compounded yearly (5,00,000 x 0.567)

4,27,700

Equity component

(Rs 5,00,000 – Rs 4,27,700) 72,300

Total proceeds 5,00,000

Note: Since Rs 105 is the conversion price of debentures into equity shares and not the redemption price, the

liability component is calculated @ Rs 100 each only.

Journal Entry

Rs Rs

Bank Dr. 5,00,000

To 8% Debentures (Liability component) 4,27,700

To 8% Debentures (Equity component) 72,300

(Being Debentures are initially recorded a fair value)

(for understanding only)

Financial Liability Account

Year Debit Amount Credit Amount

1 To bank 40,000 By Bank 4,27,700

To bal c/f 4,39,024 By interest 51,324

2 To bank 40,000 By bal b/f 4,39,024

To bal c/f 4,51,707 By interest 52,683

3 To bank 40,000 By bal b/f 4,51,707

To bal c/f 4,66,100 By interest* 54,393

23. 2