Page 8 - 23. COMPILER QB - IND AS 109_32

P. 8

Scenario (iii)

Generally, a loan which is repayable when funds are available, cannot be stated as loan repayable on demand.

Rather the entity needs to estimate the repayment date and determine its measurement accordingly by

applying the concept prescribed in Scenario

In the consolidated financial statements, there will be no entry in this regard since loan and interest

income/expense will get set off.

Scenario (iv)

In case the subsidiary YK Ltd. is planning to grant interest free loan to KK Ltd., then the difference between

the fair value of the loan on initial recognition and its nominal value should be treated as dividend distribution

by YK Ltd. and dividend income by the parent KK Ltd.

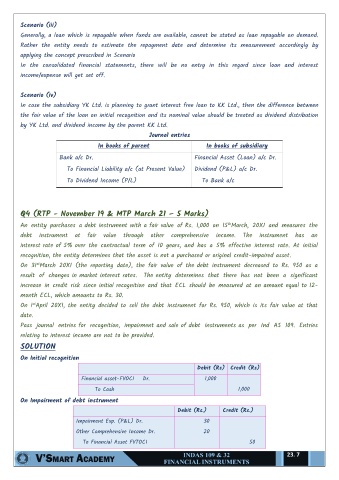

Journal entries

In books of parent In books of subsidiary

Bank a/c Dr. Financial Asset (Loan) a/c Dr.

To Financial Liability a/c (at Present Value) Dividend (P&L) a/c Dr.

To Dividend Income (P/L) To Bank a/c

Q4 (RTP - November 19 & MTP March 21 – 5 Marks)

th

An entity purchases a debt instrument with a fair value of Rs. 1,000 on 15 March, 20X1 and measures the

debt instrument at fair value through other comprehensive income. The instrument has an

interest rate of 5% over the contractual term of 10 years, and has a 5% effective interest rate. At initial

recognition, the entity determines that the asset is not a purchased or original credit-impaired asset.

On 31 March 20X1 (the reporting date), the fair value of the debt instrument decreased to Rs. 950 as a

st

result of changes in market interest rates. The entity determines that there has not been a significant

increase in credit risk since initial recognition and that ECL should be measured at an amount equal to 12-

month ECL, which amounts to Rs. 30.

st

On 1 April 20X1, the entity decided to sell the debt instrument for Rs. 950, which is its fair value at that

date.

Pass journal entries for recognition, impairment and sale of debt instruments as per Ind AS 109. Entries

relating to interest income are not to be provided.

SOLUTION

On Initial recognition

Debit (Rs) Credit (Rs)

Financial asset-FVOCI Dr. 1,000

To Cash 1,000

On Impairment of debt instrument

Debit (Rs.) Credit (Rs.)

Impairment Exp. (P&L) Dr. 30

Other Comprehensive Income Dr. 20

To Financial Asset FVTOCI 50

23. 7