Page 7 - 23. COMPILER QB - IND AS 109_32

P. 7

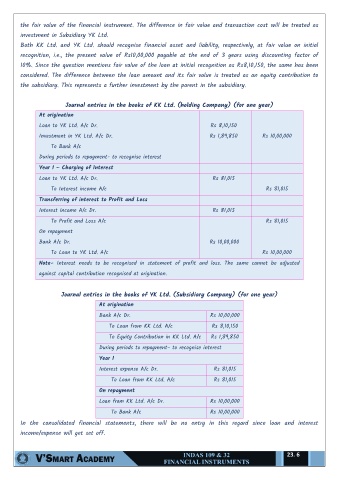

the fair value of the financial instrument. The difference in fair value and transaction cost will be treated as

investment in Subsidiary YK Ltd.

Both KK Ltd. and YK Ltd. should recognise financial asset and liability, respectively, at fair value on initial

recognition, i.e., the present value of Rs10,00,000 payable at the end of 3 years using discounting factor of

10%. Since the question mentions fair value of the loan at initial recognition as Rs8,10,150, the same has been

considered. The difference between the loan amount and its fair value is treated as an equity contribution to

the subsidiary. This represents a further investment by the parent in the subsidiary.

Journal entries in the books of KK Ltd. (holding Company) (for one year)

At origination

Loan to YK Ltd. A/c Dr. Rs 8,10,150

Investment in YK Ltd. A/c Dr. Rs 1,89,850 Rs 10,00,000

To Bank A/c

During periods to repayment- to recognise interest

Year 1 – Charging of Interest

Loan to YK Ltd. A/c Dr. Rs 81,015

To Interest income A/c Rs 81,015

Transferring of interest to Profit and Loss

Interest income A/c Dr. Rs 81,015

To Profit and Loss A/c Rs 81,015

On repayment

Bank A/c Dr. Rs 10,00,000

To Loan to YK Ltd. A/c Rs 10,00,000

Note- Interest needs to be recognised in statement of profit and loss. The same cannot be adjusted

against capital contribution recognised at origination.

Journal entries in the books of YK Ltd. (Subsidiary Company) (for one year)

At origination

Bank A/c Dr. Rs 10,00,000

To Loan from KK Ltd. A/c Rs 8,10,150

To Equity Contribution in KK Ltd. A/c Rs 1,89,850

During periods to repayment- to recognise interest

Year 1

Interest expense A/c Dr. Rs 81,015

To Loan from KK Ltd. A/c Rs 81,015

On repayment

Loan from KK Ltd. A/c Dr. Rs 10,00,000

To Bank A/c Rs 10,00,000

In the consolidated financial statements, there will be no entry in this regard since loan and interest

income/expense will get set off.

23. 6