Page 62 - 23. COMPILER QB - IND AS 109_32

P. 62

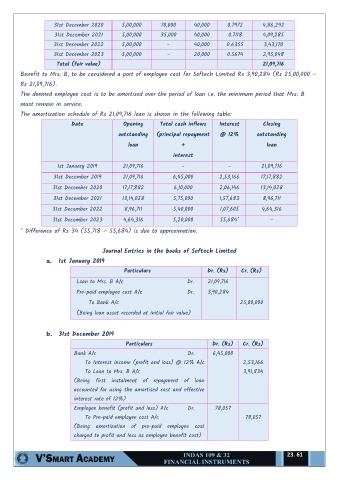

31st December 2020 5,00,000 70,000 40,000 0.7972 4,86,292

31st December 2021 5,00,000 35,000 40,000 0.7118 4,09,285

31st December 2022 5,00,000 - 40,000 0.6355 3,43,170

31st December 2023 5,00,000 - 20,000 0.5674 2,95,048

Total (fair value) 21,09,716

Benefit to Mrs. B, to be considered a part of employee cost for Softech Limited Rs 3,90,284 (Rs 25,00,000 –

Rs 21,09,716).

The deemed employee cost is to be amortised over the period of loan i.e. the minimum period that Mrs. B

must remain in service.

The amortization schedule of Rs 21,09,716 loan is shown in the following table:

Date Opening Total cash inflows Interest Closing

outstanding (principal repayment @ 12% outstanding

loan + loan

interest

1st January 2019 21,09,716 - - 21,09,716

31st December 2019 21,09,716 6,45,000 2,53,166 17,17,882

31st December 2020 17,17,882 6,10,000 2,06,146 13,14,028

31st December 2021 13,14,028 5,75,000 1,57,683 8,96,711

31st December 2022 8,96,711 5,40,000 1,07,605 4,64,316

31st December 2023 4,64,316 5,20,000 55,684* -

* Difference of Rs 34 (55,718 – 55,684) is due to approximation.

Journal Entries in the books of Softech Limited

a. 1st January 2019

Particulars Dr. (Rs) Cr. (Rs)

Loan to Mrs. B A/c Dr. 21,09,716

Pre-paid employee cost A/c Dr. 3,90,284

To Bank A/c 25,00,000

(Being loan asset recorded at initial fair value)

b. 31st December 2019

Particulars Dr. (Rs) Cr. (Rs)

Bank A/c Dr. 6,45,000

To Interest income (profit and loss) @ 12% A/c 2,53,166

To Loan to Mrs. B A/c 3,91,834

(Being first instalment of repayment of loan

accounted for using the amortised cost and effective

interest rate of 12%)

Employee benefit (profit and loss) A/c Dr. 78,057

To Pre-paid employee cost A/c 78,057

(Being amortization of pre-paid employee cost

charged to profit and loss as employee benefit cost)

23. 61