Page 63 - 23. COMPILER QB - IND AS 109_32

P. 63

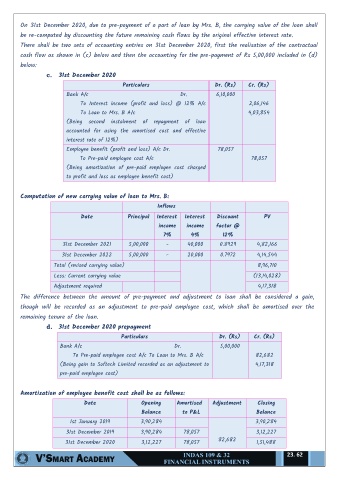

On 31st December 2020, due to pre-payment of a part of loan by Mrs. B, the carrying value of the loan shall

be re-computed by discounting the future remaining cash flows by the original effective interest rate.

There shall be two sets of accounting entries on 31st December 2020, first the realisation of the contractual

cash flow as shown in (c) below and then the accounting for the pre-payment of Rs 5,00,000 included in (d)

below:

c. 31st December 2020

Particulars Dr. (Rs) Cr. (Rs)

Bank A/c Dr. 6,10,000

To Interest income (profit and loss) @ 12% A/c 2,06,146

To Loan to Mrs. B A/c 4,03,854

(Being second instalment of repayment of loan

accounted for using the amortised cost and effective

interest rate of 12%)

Employee benefit (profit and loss) A/c Dr. 78,057

To Pre-paid employee cost A/c 78,057

(Being amortization of pre-paid employee cost charged

to profit and loss as employee benefit cost)

Computation of new carrying value of loan to Mrs. B:

Inflows

Date Principal Interest Interest Discount PV

income income factor @

7% 4% 12%

31st December 2021 5,00,000 - 40,000 0.8929 4,82,166

31st December 2022 5,00,000 - 20,000 0.7972 4,14,544

Total (revised carrying value) 8,96,710

Less: Current carrying value (13,14,028)

Adjustment required 4,17,318

The difference between the amount of pre-payment and adjustment to loan shall be considered a gain,

though will be recorded as an adjustment to pre-paid employee cost, which shall be amortised over the

remaining tenure of the loan.

d. 31st December 2020 prepayment

Particulars Dr. (Rs) Cr. (Rs)

Bank A/c Dr. 5,00,000

To Pre-paid employee cost A/c To Loan to Mrs. B A/c 82,682

(Being gain to Softech Limited recorded as an adjustment to 4,17,318

pre-paid employee cost)

Amortisation of employee benefit cost shall be as follows:

Date Opening Amortised Adjustment Closing

Balance to P&L Balance

1st January 2019 3,90,284 3,90,284

31st December 2019 3,90,284 78,057 3,12,227

82,682

31st December 2020 3,12,227 78,057 1,51,488

23. 62