Page 3 - 30. COMPILER QB - IND AS 101

P. 3

a) recognise all assets and liabilities whose recognition is required by Ind AS;

b) not recognise items as assets or liabilities if Ind AS do not permit such recognition;

c) reclassify items that it recognised in accordance with previous GAAP as one type of asset, liability or

component of equity, but are a different type of asset, liability or component of equity in accordance with

Ind AS; and

d) apply Ind AS in measuring all recognised assets and liabilities.”

Accordingly, as per the above requirements, in the given case, contributions recognised in the Capital Reserve

should be transferred to the appropriate category under ‘Other Equity’ at the date of transition to Ind AS.

Q2 (May 19)

XYZ Pvt. Ltd. is a company registered under the Companies Act, 2013 following Accounting Standards notified

under Companies (Accounting Standards) Rules, 2006. The Company has decided to voluntary adopt Ind AS

w.e.f. 1st April, 2018 with a transition date of 1st April, 2017.

The Company has one Wholly Owned Subsidiary and one Joint Venture which are into manufacturing of

automobile spare parts.

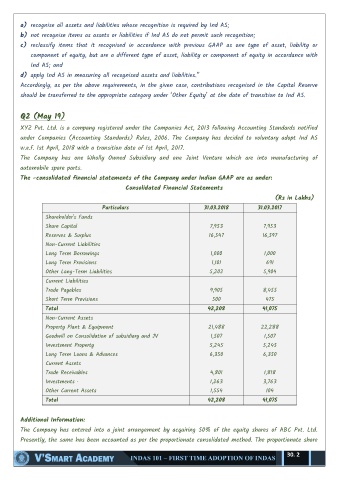

The -consolidated financial statements of the Company under Indian GAAP are as under:

Consolidated Financial Statements

(Rs in Lakhs)

Particulars 31.03.2018 31.03.2017

Shareholder's Funds

Share Capital 7,953 7,953

Reserves & Surplus 16,547 16,597

Non-Current Liabilities

Long Term Borrowings 1,000 1,000

Long Term Provisions 1,101 691

Other Long-Term Liabilities 5,202 5,904

Current Liabilities

Trade Payables 9,905 8,455

Short Term Provisions 500 475

Total 42,208 41,075

Non-Current Assets

Property Plant & Equipment 21,488 22,288

Goodwill on Consolidation of subsidiary and JV 1,507 1,507

Investment Property 5,245 5,245

Long Term Loans & Advances 6,350 6,350

Current Assets

Trade Receivables 4,801 1,818

Investments · 1,263 3,763

Other Current Assets 1,554 104

Total 42,208 41,075

Additional Information:

The Company has entered into a joint arrangement by acquiring 50% of the equity shares of ABC Pvt. Ltd.

Presently, the same has been accounted as per the proportionate consolidated method. The proportionate share

30. 2