Page 5 - 30. COMPILER QB - IND AS 101

P. 5

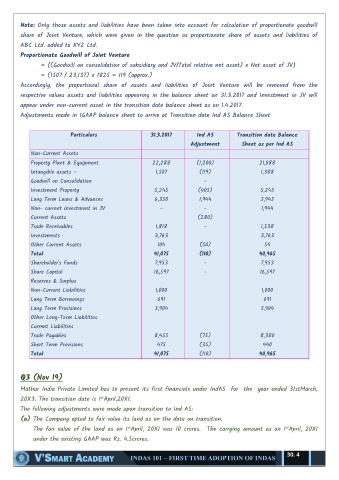

Note: Only those assets and liabilities have been taken into account for calculation of proportionate goodwill

share of Joint Venture, which were given in the question as proportionate share of assets and liabilities of

ABC Ltd. added to XYZ Ltd.

Proportionate Goodwill of Joint Venture

= [(Goodwill on consolidation of subsidiary and JV/Total relative net asset) x Net asset of JV]

= (1507 / 23,137) x 1825 = 119 (approx.)

Accordingly, the proportional share of assets and liabilities of Joint Venture will be removed from the

respective values assets and liabilities appearing in the balance sheet on 31.3.2017 and Investment in JV will

appear under non-current asset in the transition date balance sheet as on 1.4.2017.

Adjustments made in IGAAP balance sheet to arrive at Transition date Ind AS Balance Sheet

Particulars 31.3.2017 Ind AS Transition date Balance

Adjustment Sheet as per Ind AS

Non-Current Assets

Property Plant & Equipment 22,288 (1,200) 21,088

Intangible assets – 1,507 (119) 1,388

Goodwill on Consolidation -

Investment Property 5,245 (405) 5,245

Long Term Loans & Advances 6,350 1,944 5,945

Non- current investment in JV - - 1,944

Current Assets (280)

Trade Receivables 1,818 - 1,538

Investments · 3,763 3,763

Other Current Assets 104 (50) 54

Total 41,075 (110) 40,965

Shareholder's Funds 7,953 - 7,953

Share Capital 16,597 - 16,597

Reserves & Surplus

Non-Current Liabilities 1,000 1,000

Long Term Borrowings 691 691

Long Term Provisions 5,904 5,904

Other Long-Term Liabilities

Current Liabilities

Trade Payables 8,455 (75) 8,380

Short Term Provisions 475 (35) 440

Total 41,075 (110) 40,965

Q3 (Nov 19)

Mathur India Private Limited has to present its first financials under IndAS for the year ended 31stMarch,

st

20X3. The transition date is 1 April,20X1.

The following adjustments were made upon transition to Ind AS:

(a) The Company opted to fair value its land as on the date on transition.

st

st

The fair value of the land as on 1 April, 20X1 was 10 crores. The carrying amount as on 1 April, 20X1

under the existing GAAP was Rs. 4.5crores.

30. 4