Page 18 - 32. ANALYSIS OF FS

P. 18

SOLUTION

The accounting treatment made by the accountant is not in compliance with Ind AS 109 ‘Financial

Instruments’. As per Ind AS 109, at initial recognition, an entity shall measure a financial asset or financial

liability at its fair value. The fair value of a financial instrument at initial recognition is normally the

transaction price i.e. the fair value of the consideration given or received.

After initial recognition, an entity shall measure a financial asset either at amortised cost or at fair value

through profit and loss or fair value through other comprehensive income.

Here, the loan given to employee is not at market rate. Hence, the fair value of the loan will not be equal to

its initial loan proceeds. As per Ind AS 109, a financial instrument is initially measured and recorded in the

books at its fair value. Further, interest income to be recognised in the Statement of Profit and Loss will be

the finance income recognised at effective rate of interest i.e. @ 10% and not the rate of interest charged

by the company i.e. @ 6%.

The correct accounting treatment as per Ind AS 109 will be as under:

For measuring the fair value or present value of the loan at initial recognition, market rate of interest of

similar loan is considered (level 1 observable input) i.e. @ 10%, to discount the cash outflows.

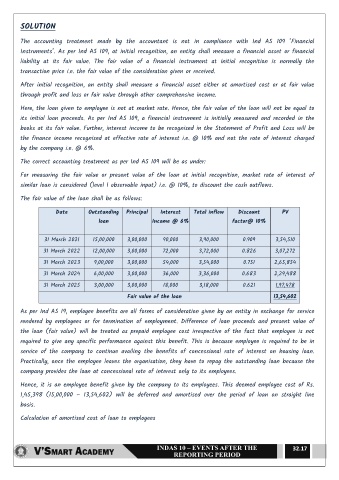

The fair value of the loan shall be as follows:

Date Outstanding Principal Interest Total inflow Discount PV

loan Income @ 6% factor@ 10%

31 March 2021 15,00,000 3,00,000 90,000 3,90,000 0.909 3,54,510

31 March 2022 12,00,000 3,00,000 72,000 3,72,000 0.826 3,07,272

31 March 2023 9,00,000 3,00,000 54,000 3,54,000 0.751 2,65,854

31 March 2024 6,00,000 3,00,000 36,000 3,36,000 0.683 2,29,488

31 March 2025 3,00,000 3,00,000 18,000 3,18,000 0.621 1,97,478

Fair value of the loan 13,54,602

As per Ind AS 19, employee benefits are all forms of consideration given by an entity in exchange for service

rendered by employees or for termination of employment. Difference of loan proceeds and present value of

the loan (fair value) will be treated as prepaid employee cost irrespective of the fact that employee is not

required to give any specific performance against this benefit. This is because employee is required to be in

service of the company to continue availing the benefits of concessional rate of interest on housing loan.

Practically, once the employee leaves the organisation, they have to repay the outstanding loan because the

company provides the loan at concessional rate of interest only to its employees.

Hence, it is an employee benefit given by the company to its employees. This deemed employee cost of Rs.

1,45,398 (15,00,000 – 13,54,602) will be deferred and amortised over the period of loan on straight line

basis.

Calculation of amortised cost of loan to employees

32.17