Page 15 - 32. ANALYSIS OF FS

P. 15

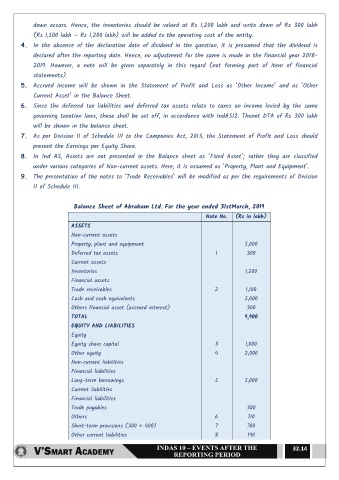

down occurs. Hence, the inventories should be valued at Rs 1,200 lakh and write down of Rs 300 lakh

(Rs 1,500 lakh – Rs 1,200 lakh) will be added to the operating cost of the entity.

4. In the absence of the declaration date of dividend in the question, it is presumed that the dividend is

declared after the reporting date. Hence, no adjustment for the same is made in the financial year 2018-

2019. However, a note will be given separately in this regard (not forming part of item of financial

statements).

5. Accrued income will be shown in the Statement of Profit and Loss as ‘Other Income’ and as ‘Other

Current Asset’ in the Balance Sheet.

6. Since the deferred tax liabilities and deferred tax assets relate to taxes on income levied by the same

governing taxation laws, these shall be set off, in accordance with IndAS12. Thenet DTA of Rs 300 lakh

will be shown in the balance sheet.

7. As per Division II of Schedule III to the Companies Act, 2013, the Statement of Profit and Loss should

present the Earnings per Equity Share.

8. In Ind AS, Assets are not presented in the Balance sheet as ‘Fixed Asset’; rather they are classified

under various categories of Non-current assets. Here, it is assumed as ‘Property, Plant and Equipment’.

9. The presentation of the notes to ‘Trade Receivables’ will be modified as per the requirements of Division

II of Schedule III.

Balance Sheet of Abraham Ltd. For the year ended 31stMarch, 2019

Note No. (Rs in lakh)

ASSETS

Non-current assets

Property, plant and equipment 5,000

Deferred tax assets 1 300

Current assets

Inventories 1,200

Financial assets

Trade receivables 2 1,100

Cash and cash equivalents 2,000

Others financial asset (accrued interest) 300

TOTAL 9,900

EQUITY AND LIABILITIES

Equity

Equity share capital 3 1,000

Other equity 4 2,000

Non-current liabilities

Financial liabilities

Long-term borrowings 5 5,000

Current liabilities

Financial liabilities

Trade payables 300

Others 6 710

Short-term provisions (300 + 400) 7 700

Other current liabilities 8 190

32.14