Page 17 - 32. ANALYSIS OF FS

P. 17

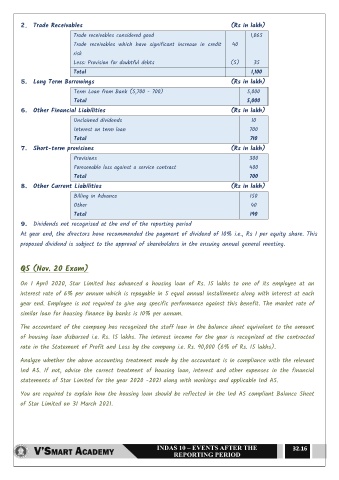

2. Trade Receivables (Rs in lakh)

Trade receivables considered good 1,065

Trade receivables which have significant increase in credit 40

risk

Less: Provision for doubtful debts (5) 35

Total 1,100

5. Long Term Borrowings (Rs in lakh)

Term Loan from Bank (5,700 - 700) 5,000

Total 5,000

6. Other Financial Liabilities (Rs in lakh)

Unclaimed dividends 10

Interest on term loan 700

Total 710

7. Short-term provisions (Rs in lakh)

Provisions 300

Foreseeable loss against a service contract 400

Total 700

8. Other Current Liabilities (Rs in lakh)

Billing in Advance 150

Other 40

Total 190

9. Dividends not recognised at the end of the reporting period

At year end, the directors have recommended the payment of dividend of 10% i.e., Rs 1 per equity share. This

proposed dividend is subject to the approval of shareholders in the ensuing annual general meeting.

Q5 (Nov. 20 Exam)

On 1 April 2020, Star Limited has advanced a housing loan of Rs. 15 lakhs to one of its employee at an

interest rate of 6% per annum which is repayable in 5 equal annual installments along with interest at each

year end. Employee is not required to give any specific performance against this benefit. The market rate of

similar loan for housing finance by banks is 10% per annum.

The accountant of the company has recognized the staff loan in the balance sheet equivalent to the amount

of housing loan disbursed i.e. Rs. 15 lakhs. The interest income for the year is recognized at the contracted

rate in the Statement of Profit and Loss by the company i.e. Rs. 90,000 (6% of Rs. 15 lakhs).

Analyze whether the above accounting treatment made by the accountant is in compliance with the relevant

Ind AS. If not, advise the correct treatment of housing loan, interest and other expenses in the financial

statements of Star Limited for the year 2020 -2021 along with workings and applicable Ind AS.

You are required to explain how the housing loan should be reflected in the Ind AS compliant Balance Sheet

of Star Limited on 31 March 2021.

32.16