Page 19 - 32. ANALYSIS OF FS

P. 19

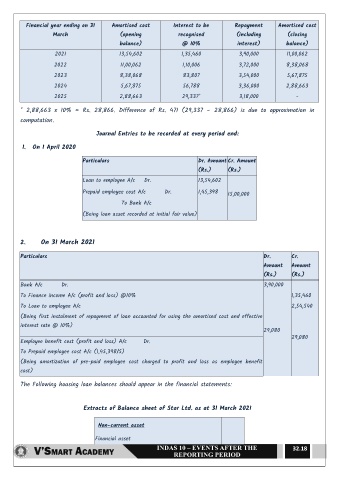

Financial year ending on 31 Amortised cost Interest to be Repayment Amortised cost

March (opening recognised (including (closing

balance) @ 10% interest) balance)

2021 13,54,602 1,35,460 3,90,000 11,00,062

2022 11,00,062 1,10,006 3,72,000 8,38,068

2023 8,38,068 83,807 3,54,000 5,67,875

2024 5,67,875 56,788 3,36,000 2,88,663

2025 2,88,663 29,337* 3,18,000 -

* 2,88,663 x 10% = Rs. 28,866. Difference of Rs. 471 (29,337 – 28,866) is due to approximation in

computation.

Journal Entries to be recorded at every period end:

1. On 1 April 2020

Particulars Dr. Amount Cr. Amount

(Rs.) (Rs.)

Loan to employee A/c Dr. 13,54,602

Prepaid employee cost A/c Dr. 1,45,398 15,00,000

To Bank A/c

(Being loan asset recorded at initial fair value)

2. On 31 March 2021

Particulars Dr. Cr.

Amount Amount

(Rs.) (Rs.)

Bank A/c Dr. 3,90,000

To Finance income A/c (profit and loss) @10% 1,35,460

To Loan to employee A/c 2,54,540

(Being first instalment of repayment of loan accounted for using the amortised cost and effective

interest rate @ 10%)

29,080

29,080

Employee benefit cost (profit and loss) A/c Dr.

To Prepaid employee cost A/c (1,45,398/5)

(Being amortization of pre-paid employee cost charged to profit and loss as employee benefit

cost)

The Following housing loan balances should appear in the financial statements:

Extracts of Balance sheet of Star Ltd. as at 31 March 2021

Non-current asset

Financial asset

32.18