Page 2 - 34.2 FR MARCH 22 MTP ANSWER

P. 2

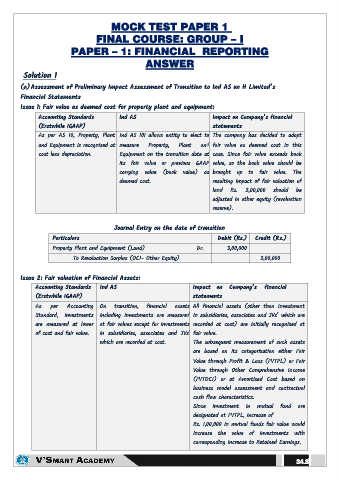

MOCK TEST PAPER 1

FINAL COURSE: GROUP – I

PAPER – 1: FINANCIAL REPORTING

ANSWER

Solution 1

(a) Assessment of Preliminary Impact Assessment of Transition to Ind AS on H Limited’s

Financial Statements

Issue 1: Fair value as deemed cost for property plant and equipment:

Accounting Standards Ind AS Impact on Company’s financial

(Erstwhile IGAAP) statements

As per AS 10, Property, Plant Ind AS 101 allows entity to elect to The company has decided to adopt

and Equipment is recognised at measure Property, Plant and fair value as deemed cost in this

cost less depreciation. Equipment on the transition date at case. Since fair value exceeds book

its fair value or previous GAAP value, so the book value should be

carrying value (book value) as brought up to fair value. The

deemed cost. resulting impact of fair valuation of

land Rs. 3,00,000 should be

adjusted in other equity (revaluation

reserve).

Journal Entry on the date of transition

Particulars Debit (Rs.) Credit (Rs.)

Property Plant and Equipment (Land) Dr. 3,00,000

To Revaluation Surplus (OCI- Other Equity) 3,00,000

Issue 2: Fair valuation of Financial Assets:

Accounting Standards Ind AS Impact on Company’s financial

(Erstwhile IGAAP) statements

As per Accounting On transition, financial assets All financial assets (other than Investment

Standard, investments including investments are measured in subsidiaries, associates and JVs’ which are

are measured at lower at fair values except for investments recorded at cost) are initially recognized at

of cost and fair value. in subsidiaries, associates and JVs' fair value.

which are recorded at cost. The subsequent measurement of such assets

are based on its categorization either Fair

Value through Profit & Loss (FVTPL) or Fair

Value through Other Comprehensive Income

(FVTOCI) or at Amortised Cost based on

business model assessment and contractual

cash flow characteristics.

Since investment in mutual fund are

designated at FVTPL, increase of

Rs. 1,00,000 in mutual funds fair value would

increase the value of investments with

corresponding increase to Retained Earnings.

34.8