Page 5 - 34.2 FR MARCH 22 MTP ANSWER

P. 5

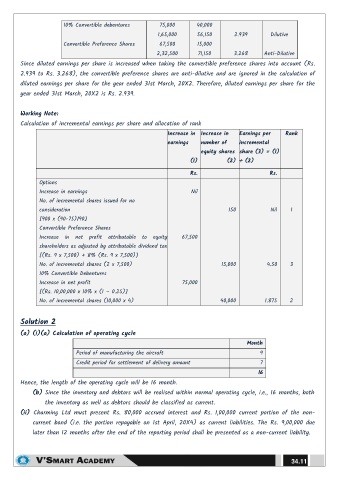

10% Convertible debentures 75,000 40,000

1,65,000 56,150 2.939 Dilutive

Convertible Preference Shares 67,500 15,000

2,32,500 71,150 3.268 Anti-Dilutive

Since diluted earnings per share is increased when taking the convertible preference shares into account (Rs.

2.939 to Rs. 3.268), the convertible preference shares are anti-dilutive and are ignored in the calculation of

diluted earnings per share for the year ended 31st March, 20X2. Therefore, diluted earnings per share for the

year ended 31st March, 20X2 is Rs. 2.939.

Working Note:

Calculation of incremental earnings per share and allocation of rank

Increase in Increase in Earnings per Rank

earnings number of incremental

equity shares share (3) = (1)

(1) (2) ÷ (2)

Rs. Rs.

Options

Increase in earnings Nil

No. of incremental shares issued for no

consideration 150 Nil 1

[900 x (90-75)/90]

Convertible Preference Shares

Increase in net profit attributable to equity 67,500

shareholders as adjusted by attributable dividend tax

[(Rs. 9 x 7,500) + 8% (Rs. 9 x 7,500)]

No. of incremental shares (2 x 7,500) 15,000 4.50 3

10% Convertible Debentures

Increase in net profit 75,000

[(Rs. 10,00,000 x 10% x (1 – 0.25)]

No. of incremental shares (10,000 x 4) 40,000 1.875 2

Solution 2

(a) (i) (a) Calculation of operating cycle

Month

Period of manufacturing the aircraft 9

Credit period for settlement of delivery amount 7

16

Hence, the length of the operating cycle will be 16 month.

(b) Since the inventory and debtors will be realised within normal operating cycle, i.e., 16 months, both

the inventory as well as debtors should be classified as current.

(ii) Charming Ltd must present Rs. 80,000 accrued interest and Rs. 1,00,000 current portion of the non-

current bond (i.e. the portion repayable on 1st April, 20X4) as current liabilities. The Rs. 9,00,000 due

later than 12 months after the end of the reporting period shall be presented as a non-current liability.

34.11