Page 4 - 34.2 FR MARCH 22 MTP ANSWER

P. 4

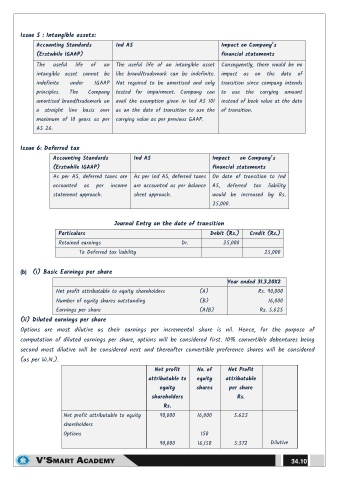

Issue 5 : Intangible assets:

Accounting Standards Ind AS Impact on Company’s

(Erstwhile IGAAP) financial statements

The useful life of an The useful life of an intangible asset Consequently, there would be no

intangible asset cannot be like brand/trademark can be indefinite. impact as on the date of

indefinite under IGAAP Not required to be amortised and only transition since company intends

principles. The Company tested for impairment. Company can to use the carrying amount

amortised brand/trademark on avail the exemption given in Ind AS 101 instead of book value at the date

a straight line basis over as on the date of transition to use the of transition.

maximum of 10 years as per carrying value as per previous GAAP.

AS 26.

Issue 6: Deferred tax

Accounting Standards Ind AS Impact on Company’s

(Erstwhile IGAAP) financial statements

As per AS, deferred taxes are As per Ind AS, deferred taxes On date of transition to Ind

accounted as per income are accounted as per balance AS, deferred tax liability

statement approach. sheet approach. would be increased by Rs.

25,000.

Journal Entry on the date of transition

Particulars Debit (Rs.) Credit (Rs.)

Retained earnings Dr. 25,000

To Deferred tax liability 25,000

(b) (i) Basic Earnings per share

Year ended 31.3.20X2

Net profit attributable to equity shareholders (A) Rs. 90,000

Number of equity shares outstanding (B) 16,000

Earnings per share (A/B) Rs. 5.625

(ii) Diluted earnings per share

Options are most dilutive as their earnings per incremental share is nil. Hence, for the purpose of

computation of diluted earnings per share, options will be considered first. 10% convertible debentures being

second most dilutive will be considered next and thereafter convertible preference shares will be considered

(as per W.N.).

Net profit No. of Net Profit

attributable to equity attributable

equity shares per share

shareholders Rs.

Rs.

Net profit attributable to equity 90,000 16,000 5.625

shareholders

Options 150

90,000 16,150 5.572 Dilutive

34.10