Page 3 - 34.2 FR MARCH 22 MTP ANSWER

P. 3

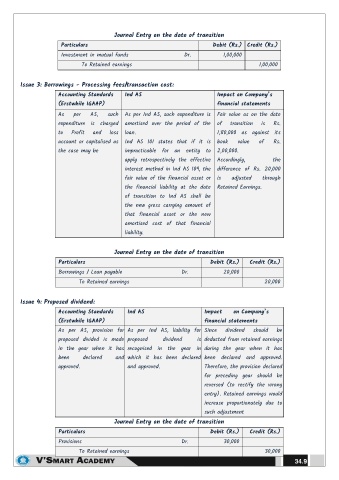

Journal Entry on the date of transition

Particulars Debit (Rs.) Credit (Rs.)

Investment in mutual funds Dr. 1,00,000

To Retained earnings 1,00,000

Issue 3: Borrowings - Processing fees/transaction cost:

Accounting Standards Ind AS Impact on Company’s

(Erstwhile IGAAP) financial statements

As per AS, such As per Ind AS, such expenditure is Fair value as on the date

expenditure is charged amortised over the period of the of transition is Rs.

to Profit and loss loan. 1,80,000 as against its

account or capitalised as Ind AS 101 states that if it is book value of Rs.

the case may be impracticable for an entity to 2,00,000.

apply retrospectively the effective Accordingly, the

interest method in Ind AS 109, the difference of Rs. 20,000

fair value of the financial asset or is adjusted through

the financial liability at the date Retained Earnings.

of transition to Ind AS shall be

the new gross carrying amount of

that financial asset or the new

amortised cost of that financial

liability.

Journal Entry on the date of transition

Particulars Debit (Rs.) Credit (Rs.)

Borrowings / Loan payable Dr. 20,000

To Retained earnings 20,000

Issue 4: Proposed dividend:

Accounting Standards Ind AS Impact on Company’s

(Erstwhile IGAAP) financial statements

As per AS, provision for As per Ind AS, liability for Since dividend should be

proposed divided is made proposed dividend is deducted from retained earnings

in the year when it has recognised in the year in during the year when it has

been declared and which it has been declared been declared and approved.

approved. and approved. Therefore, the provision declared

for preceding year should be

reversed (to rectify the wrong

entry). Retained earnings would

increase proportionately due to

such adjustment

Journal Entry on the date of transition

Particulars Debit (Rs.) Credit (Rs.)

Provisions Dr. 30,000

To Retained earnings 30,000

34.9