Page 7 - 34.2 FR MARCH 22 MTP ANSWER

P. 7

Previous GAAP revaluation, if such revaluation was, at the date of revaluation, broadly comparable to (a)

fair value or (b) cost or depreciated cost in accordance with other Ind AS adjusted to reflect changes in

general or specific price index. This measurement option can be applied on an item-by-item basis in

similar fashion as explained above.

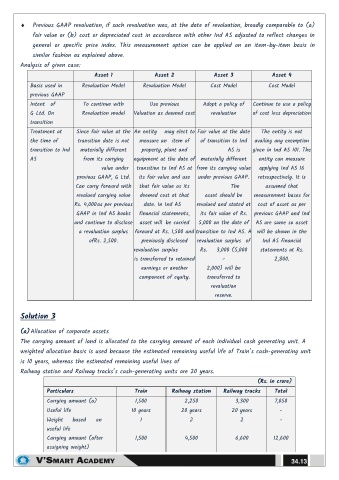

Analysis of given case:

Asset 1 Asset 2 Asset 3 Asset 4

Basis used in Revaluation Model Revaluation Model Cost Model Cost Model

previous GAAP

Intent of To continue with Use previous Adopt a policy of Continue to use a policy

G Ltd. On Revaluation model Valuation as deemed cost revaluation of cost less depreciation

transition

Treatment at Since fair value at the An entity may elect to Fair value at the date The entity is not

the time of transition date is not measure an item of of transition to Ind availing any exemption

transition to Ind materially different property, plant and AS is given in Ind AS 101. The

AS from its carrying equipment at the date of materially different entity can measure

value under transition to Ind AS at from its carrying value applying Ind AS 16

previous GAAP, G Ltd. its fair value and use under previous GAAP. retrospectively. It is

Can carry forward with that fair value as its The assumed that

revalued carrying value deemed cost at that asset should be measurement bases for

Rs. 4,000 as per previous date. In Ind AS revalued and stated at cost of asset as per

GAAP in Ind AS books financial statements, its fair value of Rs. previous GAAP and Ind

and continue to disclose asset will be carried 5,000 on the date of AS are same so asset

a revaluation surplus forward at Rs. 1,500 and transition to Ind AS. A will be shown in the

ofRs. 2,500. previously disclosed revaluation surplus of Ind AS financial

revaluation surplus Rs. 3,000 (5,000 statements at Rs.

is transferred to retained – 2,800.

earnings or another 2,000) will be

component of equity. transferred to

revaluation

reserve.

Solution 3

(a) Allocation of corporate assets

The carrying amount of land is allocated to the carrying amount of each individual cash generating unit. A

weighted allocation basis is used because the estimated remaining useful life of Train’s cash-generating unit

is 10 years, whereas the estimated remaining useful lives of

Railway station and Railway tracks’s cash-generating units are 20 years.

(Rs. in crore)

Particulars Train Railway station Railway tracks Total

Carrying amount (a) 1,500 2,250 3,300 7,050

Useful life 10 years 20 years 20 years -

Weight based on 1 2 2 -

useful life

Carrying amount (after 1,500 4,500 6,600 12,600

assigning weight)

34.13