Page 13 - 35. FR APRIL 22 MTP QP ANSWERS

P. 13

classified as item of property, plant and equipment for ` 31,70,000.

(ii) In the Consolidated Financial Statements: The consolidated financial statements present the parent and

its subsidiary as a single entity. The consolidated entity uses the building for the supply of goods.

Therefore, the leased-out property to a subsidiary does not qualify as investment property in the

consolidated financial statements. Hence, the whole building will be classified as an item of Property,

Plant and Equipment for ` 63,40,000..

(b)

(i) The Framework for integrated reporting has been written primarily in the context of private sector, for-

profit companies of any size but it can also be applied, adapted as necessary, by public sector and not-

for-profit organizations.

(ii) An integrated report may be prepared in response to existing compliance requirements. For example, an

organization may be required by local law to prepare a management commentary or other report that

provides context for its financial statements. If that report is also prepared in accordance with this

Framework, it can be considered as an integrated report. If the report is required to include specified

information beyond that required by th e Framework, the report can still be considered as an integrated

report if that other information does not obscure the concise information required by the Framework.

(c) Segment information

(A) Information about operating segment

(1) The company’s operating segments comprise:

Coatings: consisting of decorative, automotive, industrial paints and related activities.

Others: consisting of chemicals, polymers and related activities.

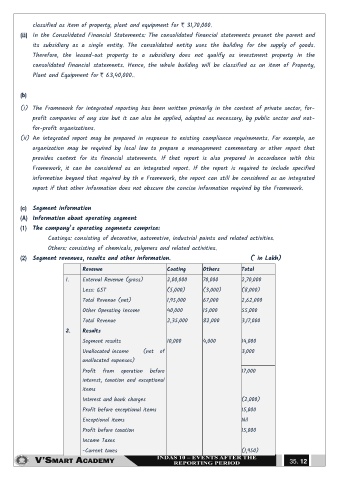

(2) Segment revenues, results and other information. (` in Lakh)

Revenue Coating Others Total

1. External Revenue (gross) 2,00,000 70,000 2,70,000

Less: GST (5,000) (3,000) (8,000)

Total Revenue (net) 1,95,000 67,000 2,62,000

Other Operating Income 40,000 15,000 55,000

Total Revenue 2,35,000 82,000 3,17,000

2. Results

Segment results 10,000 4,000 14,000

Unallocated income (net of 3,000

unallocated expenses)

Profit from operation before 17,000

interest, taxation and exceptional

items

Interest and bank charges (2,000)

Profit before exceptional items 15,000

Exceptional items Nil

Profit before taxation 15,000

Income Taxes

-Current taxes (1,950)

35. 12