Page 18 - 35. FR APRIL 22 MTP QP ANSWERS

P. 18

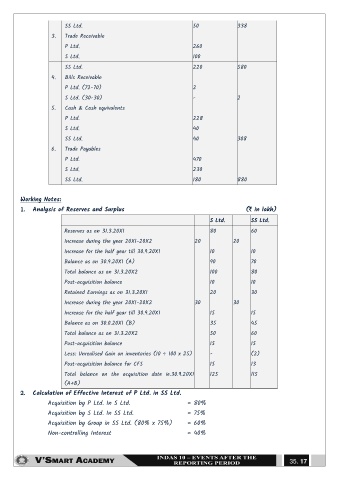

SS Ltd. 50 338

3. Trade Receivable

P Ltd. 260

S Ltd. 100

SS Ltd. 220 580

4. Bills Receivable

P Ltd. (72-70) 2

S Ltd. (30-30) - 2

5. Cash & Cash equivalents

P Ltd. 228

S Ltd. 40

SS Ltd. 40 308

6. Trade Payables

P Ltd. 470

S Ltd. 230

SS Ltd. 180 880

Working Notes:

1. Analysis of Reserves and Surplus (` in lakh)

S Ltd. SS Ltd.

Reserves as on 31.3.20X1 80 60

Increase during the year 20X1-20X2 20 20

Increase for the half year till 30.9.20X1 10 10

Balance as on 30.9.20X1 (A) 90 70

Total balance as on 31.3.20X2 100 80

Post-acquisition balance 10 10

Retained Earnings as on 31.3.20X1 20 30

Increase during the year 20X1-20X2 30 30

Increase for the half year till 30.9.20X1 15 15

Balance as on 30.0.20X1 (B) 35 45

Total balance as on 31.3.20X2 50 60

Post-acquisition balance 15 15

Less: Unrealised Gain on inventories (10 ÷ 100 x 25) - (2)

Post-acquisition balance for CFS 15 13

Total balance on the acquisition date ie.30.9.20X1 125 115

(A+B)

2. Calculation of Effective Interest of P Ltd. in SS Ltd.

Acquisition by P Ltd. In S Ltd. = 80%

Acquisition by S Ltd. In SS Ltd. = 75%

Acquisition by Group in SS Ltd. (80% x 75%) = 60%

Non-controlling Interest = 40%

35. 17