Page 14 - 35. FR APRIL 22 MTP QP ANSWERS

P. 14

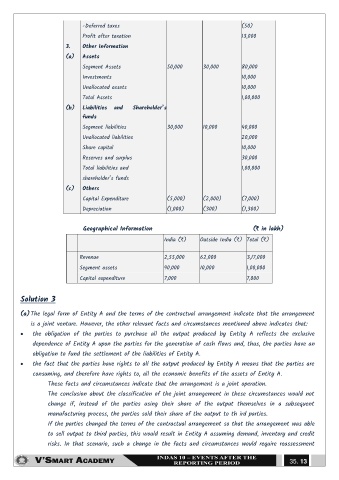

-Deferred taxes (50)

Profit after taxation 13,000

3. Other Information

(a) Assets

Segment Assets 50,000 30,000 80,000

Investments 10,000

Unallocated assets 10,000

Total Assets 1,00,000

(b) Liabilities and Shareholder’s

funds

Segment liabilities 30,000 10,000 40,000

Unallocated liabilities 20,000

Share capital 10,000

Reserves and surplus 30,000

Total liabilities and 1,00,000

shareholder’s funds

(c) Others

Capital Expenditure (5,000) (2,000) (7,000)

Depreciation (1,000) (300) (1,300)

Geographical Information (` in lakh)

India (`) Outside India (`) Total (`)

Revenue 2,55,000 62,000 3,17,000

Segment assets 90,000 10,000 1,00,000

Capital expenditure 7,000 7,000

Solution 3

(a) The legal form of Entity A and the terms of the contractual arrangement indicate that the arrangement

is a joint venture. However, the other relevant facts and circumstances mentioned above indicates that:

the obligation of the parties to purchase all the output produced by Entity A reflects the exclusive

dependence of Entity A upon the parties for the generation of cash flows and, thus, the parties have an

obligation to fund the settlement of the liabilities of Entity A.

the fact that the parties have rights to all the output produced by Entity A means that the parties are

consuming, and therefore have rights to, all the economic benefits of the assets of Entity A.

These facts and circumstances indicate that the arrangement is a joint operation.

The conclusion about the classification of the joint arrangement in these circumstances would not

change if, instead of the parties using their share of the output themselves in a subsequent

manufacturing process, the parties sold their share of the output to th ird parties.

If the parties changed the terms of the contractual arrangement so that the arrangement was able

to sell output to third parties, this would result in Entity A assuming demand, inventory and credit

risks. In that scenario, such a change in the facts and circumstances would require reassessment

35. 13